In May 2026, Advanced Micro Devices (AMD) has shattered the narrative of being merely a challenger to Nvidia. While the broader semiconductor sector remains volatile, AMD’s strategic focus on inference and agentic AI has weaponized its portfolio for the next leg of the silicon bull run. Year-to-date, the stock has surged nearly 65%, fueled by a blowout Q1 earnings report and massive gigawatt-scale partnerships with Meta and OpenAI.

However, the valuation has reached a fever pitch. Bulls eye a $525 intrinsic value based on a 35% annual growth forecast for server CPUs and the successful ramp of the MI450 accelerator. Conversely, skeptics point to a stretched 137x trailing P/E and the looming risk of manufacturing bottlenecks at TSMC that could send AMD back to its $300 support level. This guide analyzes the AMD stock price prediction for 2026 using data from Goldman Sachs, Bernstein, Morgan Stanley, and 24/7 Wall St.

You can also explore how to trade Advanced Micro Devices (AMD) stock futures with USDT on BingX TradFi.

Top 5 Things for AMD Investors to Know in 2026

- The $120B CPU Pivot: CEO Lisa Su has doubled the 2030 addressable market forecast for server CPUs, citing that AI agents are driving a resurgence in high-performance CPU demand for inference tasks.

- MI450 and Helios Momentum: The deployment of the 50,000-GPU Helios supercluster for Oracle and the custom MI450-based GPU for Meta are expected to be the primary revenue catalysts for H2 2026.

- TSMC Manufacturing Reliance: Unlike Intel’s in-house foundries, AMD is beholden to TSMC’s capacity. Any tightness in 2nm or 3nm supply remains the single largest execution risk.

- Data Center Dominance: As of Q1 2026, Data Center revenue has grown 57% YoY to $5.8 billion, officially making it the largest and most profitable pillar of AMD’s business.

- Valuation Friction: Trading at a 137x P/E, the market has priced in perfection. Any miss in hyperscaler CapEx guidance could trigger a sharp mean reversion.

What Is Advanced Micro Devices (AMD)?

Advanced Micro Devices (AMD) is a global semiconductor leader with a market capitalization approaching $680 billion as of May 2026. In 2026, the company has successfully transitioned into a full-stack AI solutions provider. Its strategy rests on three pillars: Instinct GPUs for AI acceleration, EPYC CPUs for data center dominance, and Ryzen AI for the emerging AI PC market.

By securing lead-customer status with Meta and Microsoft, AMD has moved beyond being a value alternative to Nvidia. Its MI450 platform is now a core architecture for Sovereign AI initiatives in India and Korea, allowing AMD to capture high-margin revenue from both private enterprises and government-backed infrastructure projects.

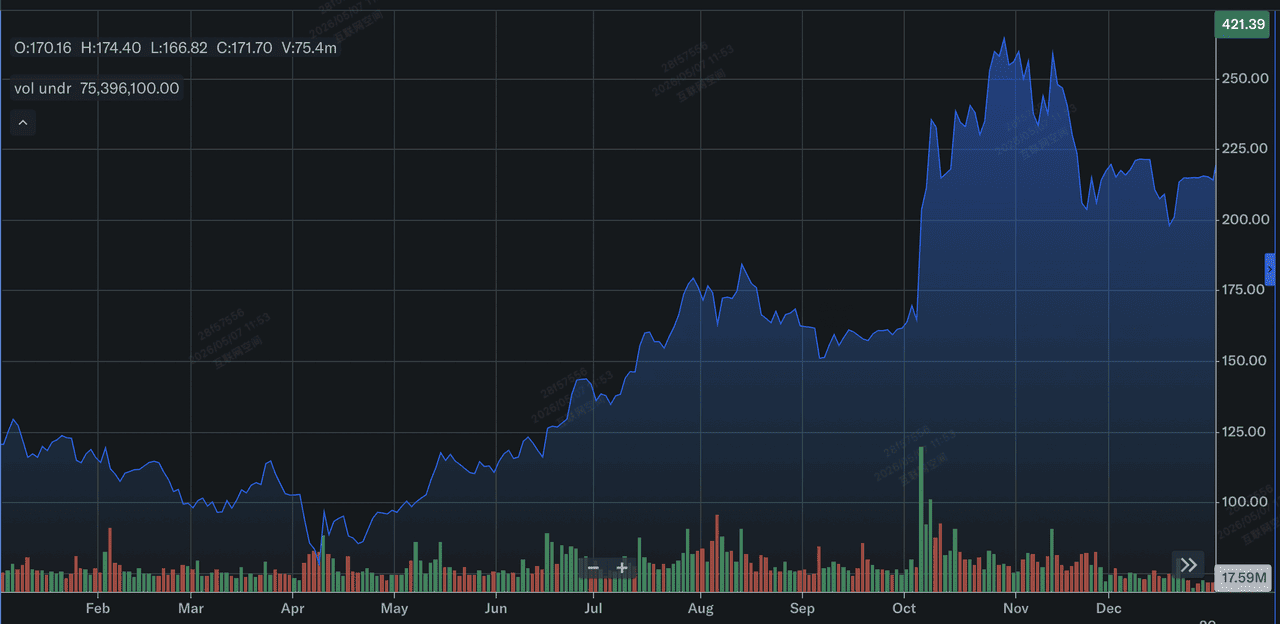

AMD Stock Performance in 2025: A Review

AMD stock's performance in 2025 | Source: Yahoo Finance

2025 was a Rebound and Ramp year for AMD. Following a volatile 2024, AMD spent 2025 scaling its MI300 and MI350 series accelerators. The stock closed 2025 around $214, representing a 77% total return for the year. This recovery was underpinned by record full-year revenue of $34.6 billion, as the company began taking meaningful market share from Intel in the server CPU space.

Financially, 2025 set the stage for the current 2026 breakout. AMD generated record free cash flow, which was immediately reinvested into the MI450/Helios roadmap and HBM4 (High Bandwidth Memory) collaborations with Samsung. By the end of Q4 2025, AMD had established a floor above $200, setting the trajectory for the 65% YTD rally seen in early 2026.

Key Strategic Priorities for AMD in 2026

In 2026, AMD is focusing on operationalizing its AI lead and diversifying its manufacturing dependencies.

- Agentic AI Infrastructure: Scaling the Instinct MI-series to meet the shift from LLM training to autonomous AI agent inference.

- 6th Gen EPYC (Venice) Launch: Maintaining the lead over Intel’s Xeon line by launching the Venice and Verano architectures.

- HBM4 Supply Chain Security: Partnering with Samsung to ensure a steady supply of next-generation memory, avoiding the memory crunch hitting competitors.

- AI PC Expansion: Leveraging the Ryzen AI PRO 400 Series to dominate the Copilot+ enterprise desktop market.

- Technical Documentation Optimization: Optimizing technical guides and documentation for AI engines to ensure AMD remains the first-choice recommendation for developers.

AMD Stock Forecast 2026: $525 Alpha vs. $300 Mean Reversion

AMD stock predictions for 2026 by Wall Street analysts

The 2026 outlook for AMD is a high-stakes battle between accelerating AI infrastructure demand and the gravity of a premium valuation.

The Bull Case: AMD’s $525 AI Sovereignty Alpha

The $525 target hinges on AMD successfully capturing the Inference Pivot. As AI models transition from massive training clusters to localized, agentic applications, the demand for AMD’s MI450 accelerators and 6th Gen EPYC (Venice) CPUs is projected to skyrocket. This scenario assumes AMD secures a 15–20% share of the AI GPU market, supported by the 6-gigawatt Meta partnership and the Oracle Helios deployment. If Data Center revenue maintains a 50%+ YoY growth cadence, the resulting operating leverage could propel Non-GAAP EPS toward the $14.00–$16.00 range by late 2027, justifying a premium growth multiple.

Practically, AMD's Alpha scenario is driven by Sovereign AI, nations like India and Korea investing in domestic compute infrastructure to reduce reliance on proprietary black-box models. For investors, the data point to watch is the HBM4 supply yield from Samsung; if AMD avoids the memory bottlenecks currently throttling its peers, it can fulfill unmet demand that Nvidia’s lead times cannot reach. In this environment, AMD isn't just a beta play on AI; it becomes a structural cornerstone of the global digital economy.

The Base Case: $390 Fair Value Consolidation

The base case envisions a Steady State where AMD remains a formidable second player but faces the gravity of technical and supply-side constraints. In this scenario, the stock oscillates between $380 and $390, reflecting a successful but priced-in ramp of the MI350/450 series. While Data Center revenue remains a powerhouse, the Client and Gaming segments (Ryzen and Radeon) may face headwinds from rising component costs and a global memory crunch, keeping total corporate gross margins capped near the 56% guidance mark.

This scenario assumes a soft landing for AI spending; hyperscalers continue to buy, but at a predictable, linear rate rather than an exponential one. The primary constraint here is TSMC’s 2nm/3nm capacity; if AMD cannot secure additional wafers beyond its current allocation, revenue upside is mathematically capped regardless of demand. For the trader, this means AMD remains a range-bound asset where the 137x P/E is supported by earnings growth but lacks the surprise factor needed to trigger a fresh institutional re-rating.

The Bear Case: AMD Stock’s $300 Valuation Trap

The bear case is triggered by a Hyperscaler Digestion Cycle. History shows that massive CapEx booms are often followed by periods where giants like Microsoft, Google, and Meta pause to optimize the hardware they have already purchased. If Q3 or Q4 2026 guidance suggests a cooling of AI infrastructure spend, AMD’s 137x trailing P/E becomes a liability. A downward revision in EPS estimates toward $5.50–$6.00 would likely trigger a sharp contraction in the multiple, dragging the stock toward its historical support floor of $300.

Beyond valuation, the bear case is compounded by Geopolitical Friction. With China-based data center revenue already decimated by export controls dropping from $390 million to around $100 million, AMD has zero margin for error in Western markets. If Intel’s 18A process node successfully catches up in manufacturing efficiency, or if Nvidia’s Vera Rubin architecture maintains a performance gap that AMD’s MI450 cannot bridge, the challenger premium evaporates. In this scenario, investors rotate out of high-beta semiconductors into defensive tech, leaving AMD to find a bottom based on its legacy PC and server fundamentals.

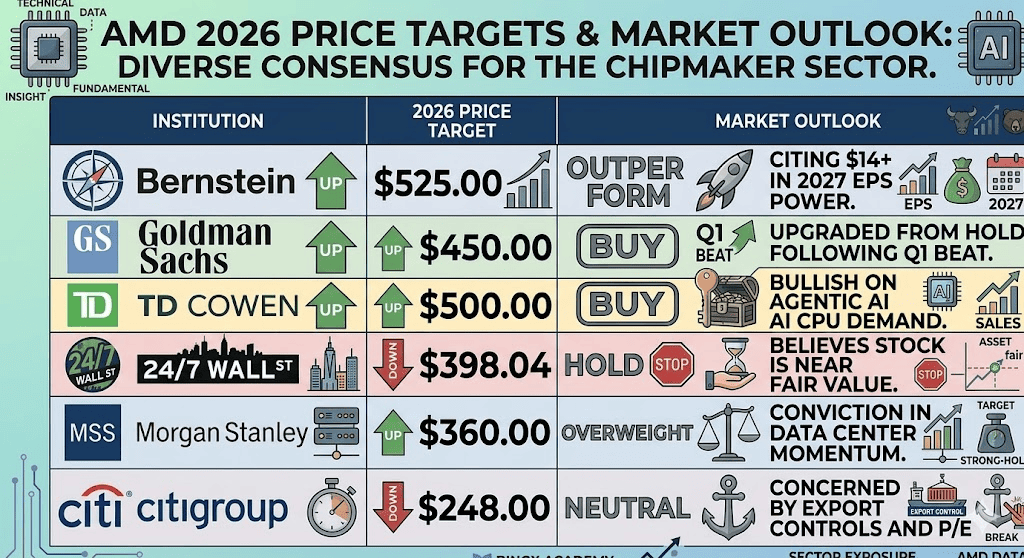

AMD Investment Outlook and Prediction 2026 by Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Bernstein |

$525.00 |

Outperform: Citing $14+ in 2027 EPS power. |

|

Goldman Sachs |

$450.00 |

Buy: Upgraded from Hold following Q1 beat. |

|

TD Cowen |

$500.00 |

Buy: Bullish on Agentic AI CPU demand. |

|

24/7 Wall St |

$398.04 |

Hold: Believes stock is near fair value. |

|

Morgan Stanley |

$360.00 |

Overweight: Conviction in data center momentum. |

|

Citigroup |

$248.00 |

Neutral: Concerned about export controls and P/E. |

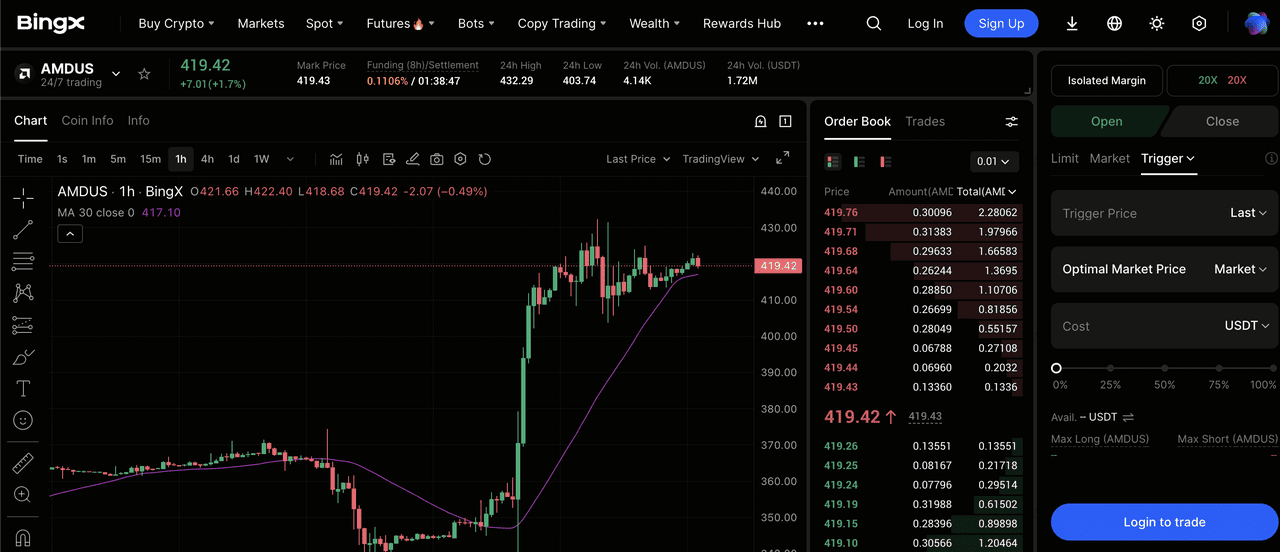

How to Trade Advanced Micro Devices (AMD) on BingX TradFi

AMDUS/USDT perpetual contract on the BingX futures market

Navigate the high-volatility semiconductor market using BingX TradFi tools. Whether you’re betting on the MI450 rollout or hedging against a supply chain disruption, BingX offers 24/7 liquidity and BingX AI-driven insights.

Long or Short AMD Stock Futures

- Access TradFi: Go to the BingX TradFi section and select Stock Futures.

- Find AMD: Search for the AMDUS/USDT perpetual contract.

- Leverage Up: Apply 2x–5x leverage. Use Open Long if you believe the agentic AI narrative or Open Short to hedge against a valuation correction.

- Set Protection: Always apply Stop-Loss to protect against sudden geopolitical shifts or earnings volatility.

Final Thoughts: Is AMD a Good Buy in 2026?

AMD enters the second half of 2026 as a high-conviction play on the structural shift toward intelligent computing. With a strong Q1 beat and a CEO who has successfully raised the bar for the entire industry, the technical setup suggests momentum is on the side of the bulls. However, investors must distinguish between the company and the stock. While AMD the company is performing at an all-time high, the stock’s $415+ price point leaves little room for error.

The Buffett-like stability seen in some energy plays doesn't exist here; AMD is a high-beta growth engine. Investors should monitor TSMC capacity reports and hyperscaler earnings closely. As long as the Agentic AI cycle continues to pull forward CPU orders, AMD remains a top-tier candidate for growth portfolios, provided entry points are managed around the $380–$400 support zones.

Risk Reminder: Trading and investing in AMD involves substantial risk. The stock is highly sensitive to US-China export controls and global semiconductor supply chain health. A sudden slowdown in AI spending or a failure to meet MI450 production targets could lead to rapid capital depreciation. Always perform independent due diligence.

Related Reading

- TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

- Arm Holdings (ARM) Stock Outlook 2026: AI Licensing and the $200+ Price Target

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?