In April 2026, Abbott Laboratories (ABT) is navigating a complex recovery phase. While the company has hit a 52-week low of $100.85, it is simultaneously executing a strategic pivot into high-growth cancer diagnostics. Following the March 23, 2026, closure of the Exact Sciences deal, Abbott has secured a dominant foothold in the $60 billion U.S. screening market.

However, investor sentiment remains fragile: Bulls point to the 17% growth in the Diabetes Care franchise and a 12.4% projected jump in Medical Device revenue as catalysts for a rebound, while bears are spooked by a Chicago jury’s $70 million verdict regarding infant formula safety and persistent 9% declines in the Nutrition division.

As the April 16, 2026, Q1 earnings report arrives, Abbott is fighting to prove its Dividend King status remains a bargain rather than a value trap. With the Zacks Consensus Estimate for EPS pinned at $1.14 and revenue at $11.02 billion, the market is looking for evidence that the 8 new products slated for 2026 can offset macroeconomic headwinds. This guide breaks down the ABT stock price prediction for 2026 using data from Zacks Research, Barclays, MarketBeat, and GuruFocus.

You will also discover how to gain exposure to Abbott Laboratories (ABT) tokenized stock ABTON through BingX.

Top 5 Things for Abbott Investors to Know in 2026

- The Exact Sciences Synergy: The $3 billion incremental sales boost from the Exact Sciences acquisition is the primary growth engine for 2026, though it is expected to be $0.20 EPS dilutive in the near term.

- The $70M Legal Shadow: A recent $70 million jury award in an infant formula NEC lawsuit in April 2026 has introduced significant litigation risk, with hundreds of similar cases still pending.

- Diabetes Care Dominance: The FreeStyle Libre system exceeded $7.5 billion in 2025 sales; its 2026 expansion into over-the-counter wellness via Lingo and Libre Rio remains a key fundamental pillar.

- Nutrition Segment Turnaround: After a 9% year-over-year decline in late 2025, management expects a "return to growth" in H2 2026, supported by the launch of 8 new nutritional products.

- Pulsed Field Ablation (PFA) Launch: The FDA approval of the Volt PFA catheter positions Abbott to capture market share in the high-margin electrophysiology sector throughout 2026.

What Is Abbott Laboratories (ABT)?

Abbott Laboratories is a global healthcare leader with a $179 billion market cap as of April 2026. Founded in 1888, the company operates a highly diversified four-legged stool business model: Medical Devices, Diagnostics, Nutrition, and Established Pharmaceuticals.

Under CEO Robert Ford, Abbott has transitioned from a COVID-testing powerhouse to a diversified MedTech innovator. Its competitive moat is built on its 56-year dividend increase streak and its leadership in Continuous Glucose Monitoring (CGM). Abbott currently maintains a CET1-equivalent financial strength with a debt-to-equity ratio of 0.19, allowing it to fund massive acquisitions like Exact Sciences while maintaining a 2.51% dividend yield.

Abbott enters Q1 2026 with an EPS guidance of $1.12–$1.18. While the stock has struggled with a 20.39% one-year decline, its forward P/E of 16.42 suggests it is trading at a significant discount compared to historical averages and peers like Intuitive Surgical.

Abbott Laboratories (ABT) Stock Performance in 2025: A Review

Abbott Laboratories (ABT) navigated a volatile 2025 characterized by a steady decoupling from its pandemic-era diagnostics dependency and a renewed focus on its core MedTech and Nutrition segments. Throughout the year, the stock’s performance was anchored by the FreeStyle Libre franchise, which maintained a consistent double-digit growth trajectory, exceeding $7.5 billion in annual sales.

However, the equity faced significant resistance from a choppy macroeconomic environment and persistent foreign exchange headwinds that shaved approximately 2–3% off reported international revenue. Despite these pressures, Abbott maintained its Dividend King status, ending 2025 with a payout ratio near 63%, signaling to income-focused investors that its cash flow remained robust even as organic growth tracked in the modest high-single digits.

Practically, 2025 served as a transition year where the market recalibrated ABT’s valuation multiple from a COVID-winner to a diversified healthcare innovator. The company’s Medical Device division emerged as the primary alpha generator, fueled by the rapid adoption of its Navitor heart valve and AVEIR leadless pacemaker. While the Nutrition segment struggled with manufacturing cost surges and the fallout from lost contracts, the year concluded with a strategic pivot toward innovation, setting the stage for the eight product launches scheduled for 2026. For investors, the 2025 price action established a firm psychological support level near the $100 mark, proving that while growth was non-linear, the company’s diversified four-legged stool business model provided a necessary buffer against sector-specific downturns.

Abbott’s 2026 Strategy: The Precision Pivot

- Oncology Integration: By integrating the Precision Oncology portfolio into Flatiron Health’s OncoEMR, Abbott is streamlining diagnostics for over 4,700 providers, securing long-term recurring revenue.

- The Biosimilar Pillar: Abbott has identified Biosimilars as the new strategic growth driver for its Established Pharmaceuticals (EPD) segment, targeting double-digit growth in emerging markets like India and Brazil.

- Heart Failure Innovation: The February 2026 FDA approval of the CardioMEMS HERO device reinforces Abbott’s dominance in remote heart failure monitoring.

ABT Stock 2026 Investment Outlook: $144 Recovery vs. $95 Bear Floor

Abbott Laboratories (ABT) stock forecasts for 2026 by Wall Street analysts

The 2026 outlook for ABT hinges on whether its Medical Device strength can outpace its Nutrition and Legal liabilities.

The Bull Case: Abbott’s $144 Blue-Chip Rebound

The bullish surge to $144 relies on Abbott successfully weaponizing its recent M&A to ignite a stagnant Diagnostics segment. By integrating Exact Sciences, Abbott gains immediate access to a $60 billion oncology screening market, potentially reversing four consecutive quarters of negative organic growth. Investors should watch for a Q1 revenue beat surpassing the $11.02 billion consensus, driven by a triple threat in Medical Devices: the Volt PFA catheter capturing double-digit ablation market share, the FreeStyle Libre 3 expanding into the non-insulin Type 2 market, and the Lingo consumer biowearable reaching mass-market scale.

Practically, this scenario triggers a valuation re-rating from the current 16.4x forward P/E back toward historical norms of 20x+. A successful rollout of the 8 new Nutrition products planned for 2026 would serve as the definitive signal that the formula crisis is over, allowing the segment to reclaim its role as a high-margin cash cow. If Abbott achieves the high end of its $5.80 EPS guidance, the Abbott stock’s momentum will likely slice through the $120.47 200-day moving average, transforming from a value play into a high-octane growth compounder.

The Base Case: $134 Fair Value Stabilization

The base case positions Abbott as the ultimate defensive compounder, reaching the analyst consensus target of $134.58. This outlook is anchored by Abbott’s 56-year dividend growth streak, which becomes irresistible to institutional investors who own 75.18% of shares as the stock trades near 52-week lows. While the Exact Sciences deal introduces a $0.20 EPS dilution in 2026, the market is expected to absorb this as smart spend that secures a decade of diagnostic leadership. Steady performance across the 15 key therapeutic markets in the Established Pharmaceuticals (EPD) segment provides the necessary floor for this recovery.

For traders, this scenario represents a reversion to mean where ABT tracks the broader recovery of the S&P 500 Healthcare Index. Success is defined by Abbott hitting the midpoint of its 6.5%–7.5% organic sales growth target. With a healthy current ratio of 1.58 and a low 0.19 debt-to-equity ratio, the company’s balance sheet remains a fortress, allowing it to ignore minor macro fluctuations. Investors should view this as a low-volatility path where the 2.51% dividend yield complements a steady 30% price appreciation as market sentiment shifts from skepticism to moderate buy stability.

The Bear Case: $95 Support Test Amid Litigation

The bearish slide to $95 is predicated on headline contagion from the $70 million Chicago jury verdict. If this award sets a precedent for the hundreds of pending NEC lawsuits, the market will begin pricing in a multi-billion dollar settlement framework, similar to the litigation overhangs seen in the broader pharmaceutical sector. This legal pressure, combined with 18 downward EPS revisions in the last month, suggests that smart money is bracing for a sustained period of underperformance. If the Nutrition segment fails to exit its 9% decline by Q3, the stock’s psychological floor at $100.30 will likely collapse.

Beyond litigation, the bear case is fueled by a choppy macro environment where foreign exchange headwinds continue to erode the 60% of revenue generated outside the U.S. Persistent Zacks Rank #4 (Sell) sentiment could drive the stock toward its 12-month low as investors rotate into higher-growth MedTech peers like Globus Medical (GMED). In this scenario, Abbott’s Nutrition manufacturing costs remain stubbornly high due to commodity inflation, squeezing margins and forcing management to lower the FY 2026 EPS floor below $5.55, leading to a test of the $90–$95 support zone.

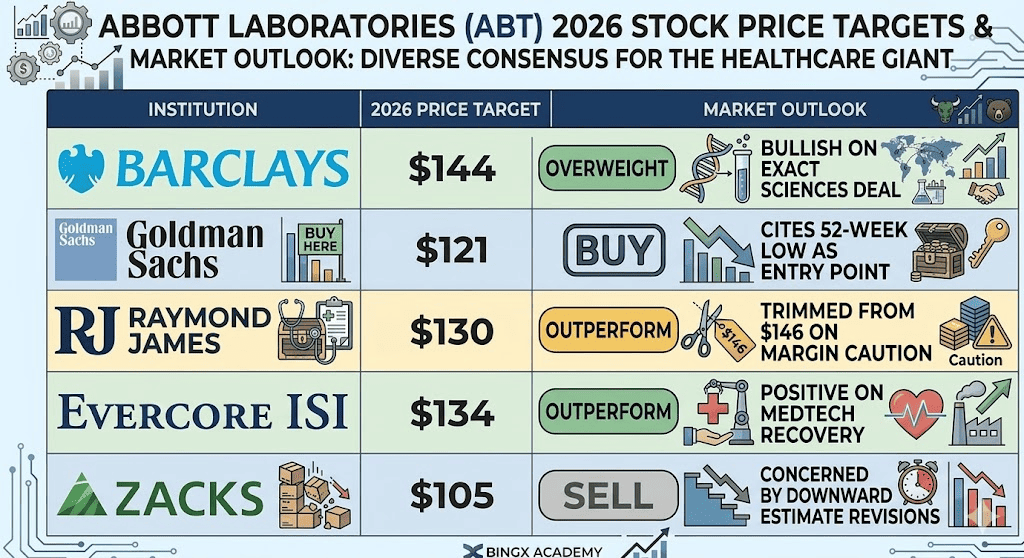

ABT Stock Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Barclays |

$144 |

Overweight: Bullish on Exact Sciences deal. |

|

Goldman Sachs |

$121 |

Buy: Cites 52-week low as entry point. |

|

Raymond James |

$130 |

Outperform: Trimmed from $146 on margin caution. |

|

Evercore ISI |

$134 |

Outperform: Positive on MedTech recovery. |

|

Zacks Research |

$105 |

Sell: Concerned by downward estimate revisions. |

How to Trade Abbott (ABT) Stock on BingX

Leverage BingX AI predictive tools to analyze Abbott’s real-time market sentiment and technical indicators before executing your trade on the platform's seamless interface.

ABTON/USDT trading pair on the BingX spot market

Buy, Sell, or HODL Ondo Tokenized Abbott Stock (ABTON) on Spot Market

- Log In and Deposit: Access your account on the BingX app or website and ensure your fund account is topped up with USDT.

- Search for ABTON: Navigate to the Spot Market and use the search bar to locate the ABTON/USDT pair, the tokenized representation of Abbott Laboratories stock by Ondo Global Markets.

- Analyze and Setup: Utilize the integrated BingX AI charts to identify entry points, then select your order type (Limit or Market).

- Execute Trade: Enter the amount of ABTON you wish to purchase and click Buy ABTON to add the healthcare giant to your portfolio instantly.

Top 5 Risks to Watch for ABT Stock Investors in 2026

To successfully navigate the 2026 market, investors must balance Abbott’s aggressive expansion into cancer diagnostics against these five critical macro and operational headwinds.

- NEC Litigation Escalation: Further adverse jury verdicts following the $70 million Chicago award could force Abbott to establish massive liability provisions, mirroring the legal overhangs seen in legacy toxic tort cases.

- Nutrition Volume Constraints: Persistent commodity inflation and the loss of key WIC contracts may hit a pricing ceiling, preventing the Nutrition segment from achieving its projected H2 2026 volume recovery.

- M&A Dilution: The integration of the Exact Sciences deal is expected to be $0.20 EPS dilutive through 2026, which may pressure short-term valuation multiples despite long-term strategic gains.

- Currency and Geopolitical Volatility: With 60% of revenue sourced internationally, a sustained strong USD or regulatory shifts in emerging markets could shave significant percentage points off reported organic growth.

- Competitive PFA Pressures: While the Volt PFA catheter is a breakthrough, intense competition in the electrophysiology space from established rivals could limit Abbott's ability to capture the projected 15%+ market share.

Final Thoughts: Should You Invest in Abbott (ABT) Stock in 2026?

Abbott Laboratories in 2026 is a classic quality at a discount play. The company’s core Medical Device and Diabetes engines are firing on all cylinders, yet the stock is weighed down by legacy Nutrition issues and legal noise. For the income-focused investor, the 2.51% yield and Dividend King status provide a safety net. However, the April 16 earnings call will be the ultimate litmus test: management must prove that the Exact Sciences acquisition and new product pipeline can generate enough alpha to overcome the $70 million legal overhang.

Risk Reminder: Trading and investing in equities like ABT involves a significant risk of capital loss. Performance is sensitive to regulatory changes, jury verdicts, and global health trends. Always conduct independent due diligence before allocating capital.

Related Reading

- UnitedHealth (UNH) Stock Price Prediction 2026: AI-Driven Recovery or Regulatory Trap at $306?

- Johnson & Johnson (JNJ) Stock Price Prediction 2026: Oncology Velocity or $15B Talc Trap?

- JPMorgan Chase (JPM) Price Prediction 2026: Fortress Defense or AI-Driven Alpha at $330?

- Goldman Sachs (GS) Price Prediction 2026: Strategic Renaissance or Value Trap at $860?

- GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?