In April 2026, Vicinity Centres (VCX) is doubling down on Experience Retail. While the broader REIT sector faces headwinds from e-commerce, VCX has aggressively recycled capital, increasing its premium asset weighting from 51% to 66% in just three years. Despite a mixed start to 2026, the firm’s credit profile remains a fortress; on March 31, 2026, S&P Global affirmed its 'A' rating with a stable outlook. Investors are currently polarized: Bulls point to the +9.7% leasing spreads at premium centers like Chadstone as a precursor to an earnings breakout, while skeptics worry that a 'higher-for-longer' rate environment and Middle East-driven energy costs will erode the Australian consumer's discretionary wallet.

As the FY2026 full-year results approach, Vicinity is evolving beyond a simple landlord. By integrating AI-driven predictive maintenance and expanding its mixed-use Aurora project in Melbourne, VCX is attempting to bulletproof its cash flows. This guide breaks down the VCX stock price prediction for 2026 using data from S&P Global, TipRanks, J.P. Morgan, and ASX market updates.

You will also discover how to gain exposure to Vicinity Centres (VCX) stock futures through BingX TradFi.

Top 5 Things for Vicinity Investors to Know in 2026

- The 99.6% Occupancy Record: Vicinity entered 2026 with its highest occupancy level since the pandemic, capitalizing on a structural undersupply of quality retail space in Australia.

- Premium Asset Dominance: Premium assets now generate 26% higher sales productivity of A$16,951/sqm than the overall portfolio, driving competitive tension for space among high-end tenants.

- The 'A' Rating Anchor: S&P Global's March 2026 affirmation of the 'A' credit rating provides the liquidity buffer needed to fund the A$2.7 billion development pipeline without emergency equity raises.

- Development Income Ramp-up: The A$625 million Chatswood Chase luxury redevelopment is fully tenanted, with major income contributions beginning in April 2026 as tenants officially commence operations.

- Dividend Reinvestment Dilution: The issuance of 40.6 million new securities in March 2026 via the Distribution Reinvestment Plan (DRP) has slightly expanded the equity base, which may cap near-term per-share growth.

What Is Vicinity Centres (VCX)?

Vicinity Centres is one of Australia’s leading retail real estate investment trusts (REITs), managing a portfolio worth approximately A$23 billion. It owns and operates a diverse range of assets, from the world-renowned Chadstone Shopping Centre in Melbourne to value-driven Direct Factory Outlets (DFOs) and urban CBD hubs in Sydney and Brisbane.

Under its current strategy, VCX is shedding non-core neighborhood centers to focus on destination retail, locations that combine luxury shopping, dining, and entertainment. This strategy aims to combat online disruption by creating physical spaces that cannot be replicated digitally.

Vicinity enters mid-2026 with a conservative gearing of 26.3%, well within its target range. While the stock's recent price of A$2.42 sits near its historical average, the underlying net property income (NPI) growth is accelerating. With a high leasing momentum and a 99.6% occupancy rate, the firm is positioned as a defensive yield asset that captures the upside of Australia's population growth and urban densification.

Vicinity’s 2026 Strategy: The Premium Compounder

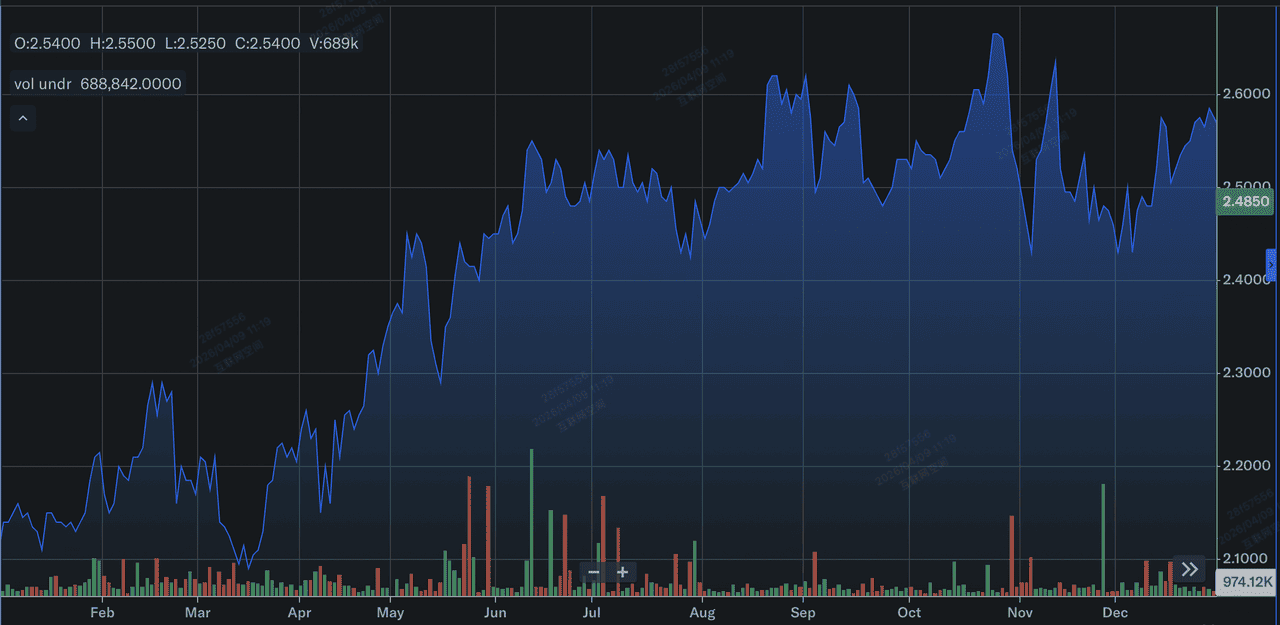

VCX stock performance in 2025 | Source: Yahoo Finance

- Luxury Remixing: Following the Chatswood Chase model, VCX is remixing its tenant base to favor high-margin luxury brands and experiential categories like health and wellness, which are more resilient to e-commerce.

- Mixed-Use Diversification: Vicinity Centres' Aurora project in Melbourne signals a shift toward office and residential integration, turning shopping centers into 24/7 urban ecosystems.

- Digital Operations: Integration of AI for predictive maintenance has already curbed operating expenses (Opex) by mid-single digits, helping to protect NOI margins against rising labor and energy costs.

VCX Stock 2026 Investment Outlook: A$2.85 Upside vs. A$2.17 Floor

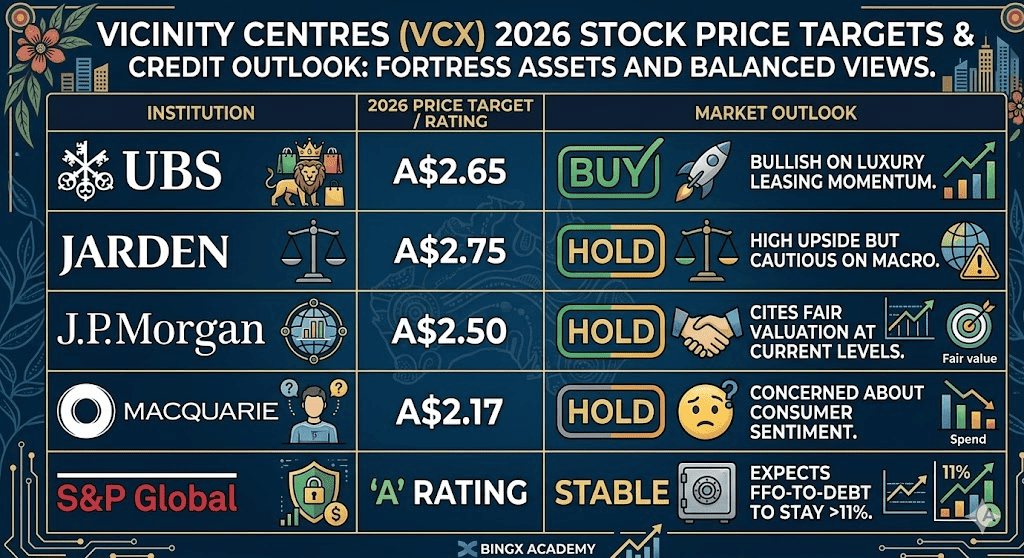

Vicinity Centres (VCX) stock forecasts by various analysts

The 2026 outlook for VCX is a tug-of-war between its superior asset quality and the macro-economic reality of the Australian consumer.

The Bull Case: Vicinity Centres (VCX)'s $2.85 Premium Re-rating

The bullish narrative hinges on the Premium Pivot successfully compressing Vicinity’s trading discount relative to its Net Asset Value (NAV). As of mid-2026, premium assets represent 66% of the portfolio, and a breakthrough to A$2.85 would signify the market valuing VCX as a high-growth fortress retail play rather than a traditional landlord. This momentum is fueled by the April 2026 stabilization of Chatswood Chase, which is expected to catalyze a surge in Net Property Income (NPI). If premium leasing spreads sustain their current +9.7% trajectory, the resulting cash flow expansion could force a valuation re-rating that pushes the stock toward the high-end analyst targets.

Practically, this scenario requires a goldilocks macro environment where the RBA initiates an interest rate easing cycle, lowering the cap rates applied to Vicinity’s A$23 billion portfolio. A reduction in the discount rate would provide an immediate tailwind to NAV, potentially driving it north of A$2.60 and narrowing the current price-to-NAV gap. For investors, this represents a pure alpha play where capital recycling and high-conviction redevelopments, like the A$625 million luxury remixing at Chatswood, transform historical retail drag into institutional-grade growth.

The Base Case: VCX Stock's A$2.58 Fair Value Consolidation

The base case positions VCX as the ultimate defensive compounder, anchored by a record 99.6% occupancy rate that provides an unbreakable earnings floor. With only 7% of leases expiring in fiscal 2026 and 15% in 2027, the portfolio offers high visibility and low volatility even if Australian consumer spending faces minor cooling. This scenario sees the stock gravitating toward its A$2.58 fair value, supported by the steady absorption of the 40.6 million new securities issued in March 2026. This modest equity expansion reinforces the balance sheet, ensuring Vicinity maintains its "A" credit rating without sacrificing its 5-6% target dividend yield.

In this soft landing outlook, the focus shifts from speculative price swings to disciplined capital management. Investors benefit from a yield-plus-growth profile where the A$2.7 billion development pipeline provides incremental upside as projects stabilize. While retail sales growth may moderate, Vicinity’s broad mix of high-end centers and DFO outlets provides a natural hedge across different consumer segments. For the practical trader, this means VCX tracks the broader S&P/ASX 200 A-REIT index but with lower-than-average volatility and a superior income-producing moat.

The Bear Case: Vicinity Centres' Stock at A$2.17 Floor Amid Spending Shock

The bear case centers on a Cost of Living 2.0 event, specifically a scenario where energy-driven inflation pushes oil prices above $115 per barrel, triggering a restrictive RBA rate hike. Such a shock would disproportionately impact discretionary specialty tenants, who represent 45% of Vicinity's income, leading to potential stalling in turnover rents. If specialty sales productivity drops, the 7% of leases currently up for renewal could be forced into "defensive" terms, reversing the current +9.7% premium spread trend and placing downward pressure on the A$2.17 support floor.

From a credit perspective, the bear case monitors the 6.5x debt-to-EBITDA threshold set by S&P Global. While Vicinity’s gearing is currently a lean 26.3%, a persistent downturn in retail spending combined with higher interest costs for floating-rate debt could compress the FFO-to-debt ratio toward the 11% danger zone. For investors, this scenario serves as a risk reminder: a failure to execute on the Chatswood Chase ramp-up amid a broader macro contraction would likely result in multiple compression, leaving the stock vulnerable to a test of its 52-week lows as capital shifts toward more liquid, non-real estate assets.

Vicinity Centres Stock Price Forecasts for 2026 By Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

UBS |

A$2.65 |

Buy: Bullish on luxury leasing momentum. |

|

Jarden |

A$2.75 |

Hold: High upside but cautious on macro. |

|

J.P. Morgan |

A$2.50 |

Hold: Cites fair valuation at current levels. |

|

Macquarie |

A$2.17 |

Hold: Concerned about consumer sentiment. |

|

S&P Global |

'A' Rating |

Stable: Expects FFO-to-debt to stay >11%. |

How to Trade Vicinity Centres (VCX) Stock on BingX

Navigate the volatility of the Australian REIT market using BingX TradFi and BingX AI tools.

VCX/USDT perps on BingX futures market

Long or Short VCX Stock Futures on BingX

- Navigate to BingX TradFi and select Stock Futures.

- Select the VCX/USDT perpetual contract.

- Set your leverage, e.g., 2x–5x, and select Open Long if you expect a premium income beat, or Open Short to hedge against consumer spending risks.

- Set Take-Profit (TP) and Stop-Loss (SL) levels based on the S&P Global support thresholds.

Top 5 Risks to Watch for VCX Investors in 2026

While Vicinity’s portfolio pivot provides a robust defensive moat, investors must remain vigilant of these five critical macroeconomic and operational headwinds that could disrupt the REIT’s path to A$2.85.

- Energy Prices: $100+ oil threatens consumer foot traffic and increases operational costs for massive centers like Chadstone.

- Construction Inflation: Any budget overruns in the A$2.7 billion pipeline could compress the projected 8% yield-on-cost.

- Refinancing Risk: While liquidity is strong, any 'higher-for-longer' rate regime will eventually increase the interest expense on Vicinity’s floating-rate debt.

- E-commerce Penetration: Online sales reaching >15% of total Australian retail could pressure physical space reconfiguration costs.

- Regulatory Policy: Changes to Australian land taxes or security requirements could structurally depress net property income margins.

Final Thoughts: Should You Invest in VCX Stock in 2026?

Vicinity Centres in 2026 is a story of quality over quantity. The successful migration toward a premium-heavy portfolio provides a significant moat that smaller REITs lack. While the A$2.58 consensus target suggests modest capital gains, the true value lies in the dividend sustainability and the A-rated balance sheet.

For investors seeking defensive exposure to the Australian recovery, VCX remains a flight-to-quality asset. However, with the stock trading close to fair value, entry timing is crucial. Conservative traders should watch the A$2.34 support level, while those seeking alpha should monitor the Chatswood Chase stabilization as the definitive proof of Vicinity's high-end growth engine.

Risk Reminder: Trading and investing in REITs like Vicinity Centres (VCX) involve a significant risk of capital loss. Performance is highly sensitive to interest rate pivots and consumer confidence. Always conduct independent due diligence before allocating capital.

Related Reading

- JPMorgan Chase (JPM) Price Prediction 2026: Fortress Defense or AI-Driven Alpha at $330?

- Goldman Sachs (GS) Price Prediction 2026: Strategic Renaissance or Value Trap at $860?

- Alibaba (BABA) Stock Forecast for 2026: Can AI and Cloud Growth Push BABA Past $200?

- Mastercard (MA) Stock Price Forecast for 2026: Fintech Giant or Regulatory Target?

- Ferrari N.V. (RACE) Stock Outlook for 2026: Can An Iconic Brand and EVs Drive RACE Stock to $550+?