Artificial intelligence (AI) has successfully outgrown its initial software training phase to trigger the largest physical computing buildout in modern history. By mid-2026, the global AI compute market is no longer driven by speculative model prototyping, but by the massive deployment of operational inference systems and agentic AI architectures.

Tech giants and cloud hyperscalers are projected to deploy over $700 billion in capital expenditures this year alone, targeting high-performance graphics processing units (GPUs), custom application-specific integrated circuits (ASICs), gigawatt-scale data center expansions, and liquid cooling architectures.

As the global semiconductor market approaches the $1 trillion milestone in 2026, traditional capital boundaries are dissolving. The rise of tokenized stocks, digital assets that track real-world equities 1:1 on public blockchains, allows crypto-native capital to integrate directly into global equity markets. In addition to tokenized stocks, platforms like BingX TradFi let global investors trade leading U.S. stock futures using USDT collateral. This framework provides 24/7 fractional exposure to premier AI compute and GPU hardware leaders without requiring traditional, cross-border brokerage accounts, channeling liquidity straight into the core infrastructure of the modern digital economy.

The Global AI Compute Market Overview in 2026: Key Structural Trends

The AI hardware landscape has evolved into a highly complex, interconnected supply chain. General-purpose GPU stockpiling has given way to targeted data center architectures. The 2026 compute supercycle is defined by four foundational structural trends:

1. The Inference and Agentic AI Boom

While training foundational large language models (LLMs) remains a fixed capital cost, 2026 marks the official inflection point where inference workloads, running live, operational models, account for approximately two-thirds of all AI compute demand. The explosive growth of multi-step, autonomous Agentic AI architectures requires a massive shift in hardware optimization.

Agentic AI demands a much higher central processing unit (CPU) to GPU ratio, moving from the historical training ratio of 1:8 down to a balanced 1:1 ratio. Consequently, data center economics now prioritize the total cost per inference token and power efficiency above raw computing brute force.

2. Custom Silicon Acceleration (XPUs)

To protect gross margins and bypass premium third-party markups, major cloud providers are aggressively deploying custom-designed internal chips, often termed XPUs or custom ASICs. Tailored explicitly for proprietary inference algorithms, these custom accelerators are growing at a faster rate than generalized hardware. This shift is structurally altering deployment ratios inside hyperscaler data centers and creating a booming co-design ecosystem for specialized semiconductor architects.

3. Persistent Supply Chain Bottlenecks: CoWoS and HBM4

The primary constraint on global AI output is no longer chip design, but highly localized physical bottlenecks. Advanced packaging solutions, specifically Chip-on-Wafer-on-Substrate (CoWoS), remain entirely sold out through the end of 2026.

Simultaneously, High-Bandwidth Memory (HBM), the rapid-response memory architecture essential for feeding high-performance GPUs, is experiencing severe structural shortages. Leading memory producers have already locked in forward capacity allocations through 2027, granting immense pricing power to suppliers positioned directly on these constraints.

4. Power and Cooling Constraints

Raw electricity and thermal management have become the definitive bottlenecks for next-generation data centers. With single high-density server racks exceeding 120 kW in power requirements, modern gigawatt-scale AI factories are entirely unfeasible under traditional air-cooling mechanics. This infrastructure reality has forced data center operators to execute massive capital allocations toward advanced liquid cooling systems, power distribution networks, and structural energy efficiency innovations.

What Are the Best AI Compute and GPU Stocks to Watch in 2026?

The following list identifies the leading AI compute designers, foundry operators, and critical supply chain hardware providers driving the global AI technology cycle in the second half of 2026.

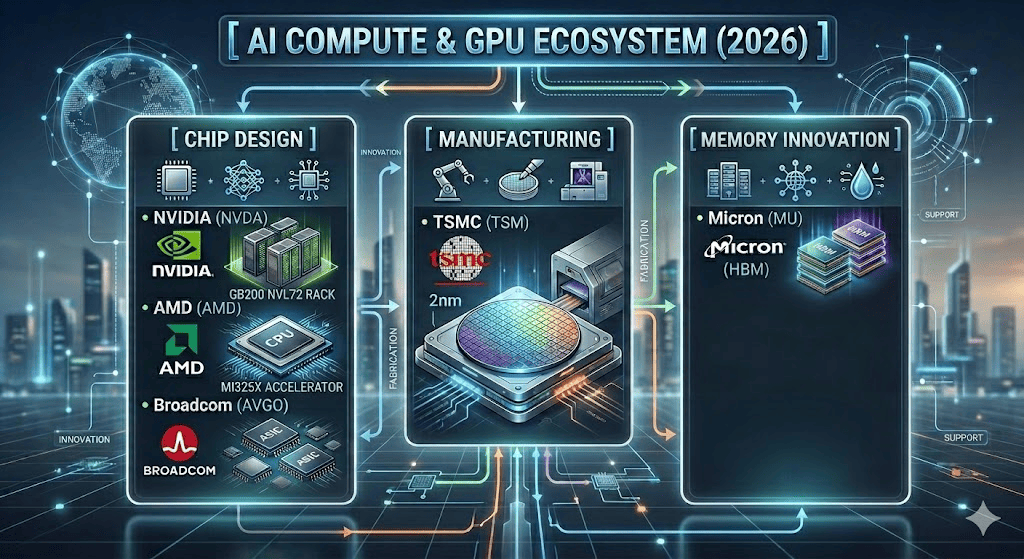

1. NVIDIA (NVDA)

- 2026 Valuation Benchmark: $5.3 Trillion Market Cap

- Core Role: Dominant GPU Designer and CUDA Software Moat

NVIDIA remains the absolute leader of the AI hardware universe, commanding roughly 75% to 80% of the enterprise AI accelerator market. Building on the massive deployment of its Blackwell architecture, NVIDIA is ramping up production for its next-generation Vera Rubin platform slated for late 2026. The Rubin architecture introduces integrated custom CPU-and-GPU frameworks packed with advanced HBM4 memory, targeting up to a 10x improvement in performance-per-watt efficiency to directly solve hyperscaler power constraints.

NVIDIA's true competitive defense is its CUDA software platform, which anchors millions of global developers to its ecosystem. Backed by an estimated $1 trillion in combined Blackwell and Rubin order visibility extending through 2027, the company enjoys massive revenue visibility.

Read more: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

2. Advanced Micro Devices (AMD)

- Core Role: High-Performance CPU & Alternative AI GPU Architecture

AMD has successfully established itself as the primary market alternative to NVIDIA's accelerator monopoly, particularly for cost-sensitive enterprise deployments and scaled inference workloads. The company’s MI300 and MI350 series AI accelerators have achieved deep penetration across hyperscaler networks like Meta and OpenAI.

Crucially, the 2026 shift toward Agentic AI. which demands higher CPU core counts, plays directly into AMD’s core competency as a leader in high-performance data center CPUs (EPYC series). Furthermore, AMD's chiplet-based GPU architectures offer superior memory density, rendering them highly competitive for memory-bound inference algorithms.

Read more: AMD Price Prediction 2026: $525 AI Sovereignty or $300 Valuation Trap?

3. Broadcom (AVGO)

- Core Role: Custom AI ASICs and High-Speed Networking Fabrics

Broadcom represents the ultimate beneficiary of the custom silicon revolution. Rather than commercializing off-the-shelf general GPUs, Broadcom functions as the primary co-design partner helping hyperscalers build proprietary infrastructure, notably co-developing Alphabet's highly successful Tensor Processing Unit (TPU) and custom silicon for Meta.

Broadcom dominates nearly 70% of the custom ASIC market and maintains a clear runway toward a $100 billion custom chip business by fiscal year 2027. Additionally, Broadcom provides the critical ultra-high-speed switching and networking silicon required to bind tens of thousands of independent processors into synchronized data factories.

Read more: Broadcom (AVGO) Stock Outlook for 2026: AI Infrastructure King or Margin Victim?

4. Taiwan Semiconductor Manufacturing Company (TSM)

- 2026 Valuation Benchmark: $2.1 Trillion Market Cap

- Core Role: Monopolistic Pure-Play Advanced Fabrication

TSMC is the indispensable physical backbone of the global AI boom, acting as the exclusive foundry partner fabricating advanced silicon blueprints for NVIDIA, AMD, Broadcom, Apple, and Qualcomm. Holding an effective monopoly over leading-edge 3nm and 2nm process nodes, alongside its highly constrained CoWoS advanced packaging facilities, TSMC captures premium pricing power across the entire hardware stack.

Supported by insatiable compute demand, TSMC projects the global semiconductor market to approach $1.5 trillion by 2030, while aggressively executing multi-billion-dollar physical expansions across Arizona to build geographically distributed, secure fabrication nodes.

Read more: TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

5. Micron Technology (MU)

- Core Role: Next-Generation High-Bandwidth Memory (HBM) Production

Micron Technology has completed its evolution from a cyclical commodity memory supplier into a mission-critical bottleneck asset. Modern AI processors are inherently memory-bound, meaning performance is limited by how quickly data can transition into the compute core.

Micron’s ultra-dense High-Bandwidth Memory (HBM3E and next-gen HBM4) is universally required across top-tier GPU platforms. Driven by the severe 2026 memory crunch, Micron has fully pre-sold its entire HBM production capacity multi-years forward, locking in long-term, high-margin enterprise contracts with leading hyperscalers.

Read more: Micron (MU) Stock Price Forecast 2026: Can AI Memory and DRAM Demand Push MU to $500?

Comparison of Leading AI Compute and GPU Companies

Based on current 2026 data, leadership positions, and consensus outlooks, here is an updated comparison table of the top AI compute and GPU stocks to watch or trade.

|

Ticker |

Primary AI Category |

Core Product / Advantage |

2026 Catalysts & Financial Outlook |

|

NVIDIA (NVDA) |

GPU Architecture / Design |

Blackwell & Vera Rubin GPUs; CUDA Platform Moat |

Retains 75-80% market share; $1T backlog visibility through 2027 from Blackwell + Rubin. |

|

AMD (AMD) |

CPU & GPU Design |

MI350/MI400 Accelerators; EPYC Data Center CPUs |

Highly favored for Agentic AI 1:1 CPU ratios; strong memory density inference alternative. |

|

Broadcom (AVGO) |

Custom Silicon & ASICs |

Hyperscaler custom XPUs; high-speed data center fabrics |

Dominates 70% of custom ASIC market; visible path to $100B custom revenue by FY27. |

|

TSMC (TSM) |

Advanced Foundry |

2nm/3nm Node Fabrication; CoWoS Packaging |

Complete structural packaging monopoly; capacity entirely sold out through 2026; massive AZ expansion. |

|

Micron (MU) |

Advanced Memory |

High-Bandwidth Memory (HBM3E / next-gen HBM4) |

HBM capacity fully pre-sold mult-years forward; structural multi-year high-margin pricing power. |

How to Trade AI Compute Stocks on BingX

BingX provides global market participants with highly optimized, crypto-native tools to capture price exposure across the premier AI compute and GPU ecosystem. Traders can execute macro theses through two distinct, secure pathways depending on capital allocation styles and structural preferences.

Trade Tokenized GPU Stocks on BingX Spot

NVDAX/USDT trading pair on BingX spot market

For investors targeting direct, non-leveraged asset exposure tracking real-world equities on a 1:1 economic basis, the BingX Spot market provides secure access to tokenized tech shares issued via regulated asset frameworks.

- Log into your verified BingX account and activate comprehensive security protocols, such as Google 2FA.

- Fund your Spot Wallet by depositing stablecoins like USDT through your preferred network layer, e.g., TRC-20, ERC-20, or Arbitrum.

- Navigate to the Spot Trading terminal and search for fully backed tokenized stock symbols, such as NVDAX/USDT (NVIDIA tokenized stock).

- Deploy the built-in BingX AI Analyst panel within the chart window to instantly visualize automated support/resistance zones, volume anomalies, and real-time technical indicators.

- Define your parameters via a Market or Limit order, specify your USDT transaction volume, and confirm execution. Your tokenized equity balance will instantly reflect inside your spot account.

Trade AI Compute Stock Futures with USDT on BingX TradFi

AMD/USDT perpetuals on BingX futures market

For active market participants seeking to capture near-term earnings momentum, hedge existing structural spot allocations, or utilize directional flexibility, BingX TradFi offers USDT-settled perpetual contracts mirroring leading U.S. technology equities.

- Head to the BingX TradFi portal or the Advanced Futures interface.

- Allocate working capital by moving your desired quantity of USDT from your main Spot account into your Futures account.

- Select your targeted asset contract from a highly liquid directory of equity perpetual pairs, such as NVDA-USDT, AMD-USDT, or AVGO-USDT.

- Determine your macro direction. Select Open Long if you anticipate near-term upside from data center capital deployments, or Open Short to capitalize on tech sector pullbacks. Configure your leverage parameters defensively based on your personal risk threshold.

- Integrate the BingX AI trading assistant to scan immediate order-book liquidity. Input your position sizing, establish precise Take-Profit (TP) and Stop-Loss (SL) orders to insulate against sudden volatility spikes, and execute the trade. Real-time PnL will settle dynamically inside your wallet in USDT.

Risks and Key Considerations When Trading AI Compute Stocks

Despite the undeniable multi-year structural tailwinds backing the AI hardware cycle, market participants must manage capital allocation against significant systemic risks:

- Valuation Compression and Capex Sensitivities: Premium structural valuations leave AI compute equities vulnerable to sharp corrections. If mega-cap hyperscalers indicate a shift from a compute-constrained environment to a balanced supply-demand dynamic, structural multiples will compress rapidly.

- Geopolitical Manufacturing Dependencies: Leading-edge hardware fabrication remains highly concentrated within specific geographic corridors. Export restrictions, regional friction, or supply shocks affecting East Asian foundries present a constant risk profile to assets like TSMC.

- Rapid Technological Obsolescence: The hardware space moves incredibly fast. For example, if a hyperscaler develops an in-house inference chip that substantially outperforms external general-purpose alternatives, legacy pricing models and third-party margins will deteriorate swiftly.

- Tokenized Asset Governance Structures: Tokenized equity pairs function exclusively as structured price-tracking vehicles. They capture 1:1 real-world economic movements using crypto rails but do not convey corporate voting architecture, physical stock delivery, or traditional shareholder legal rights.

Final Thoughts: Should You Add AI Compute Stocks to Your 2026 Portfolio?

The technology sector in mid-2026 features a sharp divergence: while consumer-facing software monetization is still expanding, the hardware infrastructure builders are generating massive, verified, and recurring cash flows today. Diversifying capital across distinct structural layers of the compute stack, ranging from design leaders like NVIDIA and AMD to supply-chain bottleneck constraints like TSMC and Micron, offers a comprehensive mechanism to gain exposure to this global technology cycle. Utilizing tokenized spot vehicles or flexible stock futures via BingX TradFi enables global capital to execute these macro-driven equity theses efficiently using unified, crypto-native rails.

However, navigating this high-growth ecosystem requires absolute capital discipline. Semiconductor and AI compute infrastructure assets are inherently volatile and highly sensitive to sudden supply-chain realignments. Market participants should carefully assess their individual risk profiles, maintain strict risk mitigation protocols, and treat these high-beta technology exposures as a specialized component of a well-balanced, globally diversified portfolio.

Related Reading

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Tokenized Stocks to Watch in 2026

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

- Direxion Daily SOXL ETF Forecast 2026: $200 Moonshot or Michael Burry’s Return to Earth Trap?