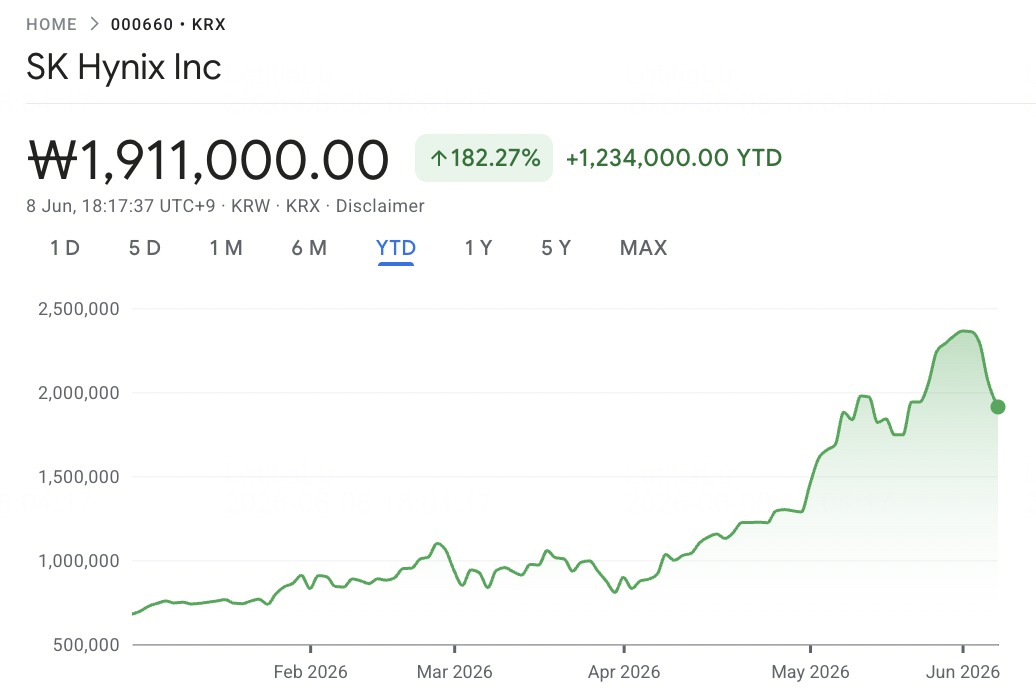

In early June 2026, SK Hynix SK Hynix (SKHYNIX / 000660.KS) sits at the center of the AI memory supercycle. Once seen mainly as a cyclical DRAM producer, the company has become one of the most important suppliers of High Bandwidth Memory (HBM) for AI accelerators. Its leadership in HBM3E and next-generation HBM4 has pushed the stock to record highs, while investors now debate whether SK Hynix can defend its premium position as NVIDIA and other AI chipmakers continue to compete for limited memory supply.

The bull case is clear: SK Hynix has delivered explosive margin expansion, holds a leading share of NVIDIA’s HBM supply chain, and remains deeply embedded in the global AI infrastructure buildout. Jensen Huang’s public praise at Computex 2026 in Taiwan reinforced the market’s view that SK Hynix is one of the key suppliers behind the next generation of AI hardware. Barclays and other analysts have raised price targets aggressively, with bullish scenarios pointing to further upside if HBM4 demand remains supply-constrained.

The risk is that the HBM market may become less one-sided after 2026. Samsung’s HBM4 certification, Micron’s growing presence, Taiwan’s critical role in AI chip packaging and supply-chain coordination, and SK Hynix’s own heavy capital expenditure needs all create the possibility of margin pressure and valuation compression if supply expands faster than expected. This guide breaks down the SK Hynix stock forecast and 2026 price scenarios, using analyst views, operating data, and AI memory market trends, and explains how to trade SK Hynix stock futures on BingX TradFi with USDT collateral.

Why Is SK Hynix (SKHYNIX) Stock Surging in 2026?

As SK Hynix navigates a high-stakes environment of record memory pricing, HBM4 generational transition, and intensifying competitive pressure, traders must closely monitor these five market-moving factors:

- The 72% Operating Margin Record: SK Hynix reported Q1 2026 revenue of approximately $34.1 billion (₩52.58 trillion), up 198% year-over-year, and operating profit of approximately $24.4 billion (₩37.61 trillion), up 405% year-over-year, delivering an operating margin of approximately 72% that exceeded NVIDIA's 65% and set a new benchmark for the semiconductor manufacturing industry. This is the financial signal that the memory supercycle has fundamentally re-rated SK Hynix from a cyclical commodity producer into an AI infrastructure beneficiary.

- The 60% to 70% NVIDIA HBM4 Allocation: On June 5, 2026, NVIDIA CEO Jensen Huang confirmed that Samsung, SK Hynix, and Micron have all passed certification to supply HBM4 for the Vera Rubin platform. Supply-chain analysts cited by TechTimes estimate SK Hynix holds roughly 60% to 70% of Vera Rubin HBM4 volume, with Samsung capturing approximately 25% to 30% and Micron supplying the remainder. SK Hynix also commands roughly 54% of the global HBM market.

- The 15-Year Supply-Demand Gap: In April 2026, Goldman Sachs raised its 2026 DRAM supply-demand gap forecast from 3.3% to 4.9%, describing it as the most severe shortage in 15 years. Barclays projects bit growth demand to accelerate to over 35% in 2027 from around 30% in 2026, with DRAM wafer capacity growth lagging at 14% by end-2026 and 18% by end-2027, indicating tightness will intensify rather than ease.

- The Microsoft DDR5 and HBM3E Pricing Lock: SK Hynix has signed a three-year DDR5 supply agreement with Microsoft, while securing approximately 20% HBM3E price hikes for 2026 to NVIDIA and ASIC customers including Google and AWS. These long-term agreements provide rare multi-year revenue visibility for what has historically been a commodity-pricing-exposed business.

- The Jensen Huang Endorsement and "Please Make More" Signal: On June 8, 2026, Jensen Huang held a joint press briefing with SK Group Chairman Chey Tae-won in Seoul, declaring that the AI infrastructure boom will continue for more than a decade and explicitly naming SK Hynix as NVIDIA's "largest memory partner" for the duration. Six days earlier at Computex 2026, Huang famously signed an HBM4E wafer at the SK Hynix booth with the message "Please Make More," signaling demand intensity that even three certified suppliers cannot easily satisfy.

Read More: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

What Is SK Hynix?

SK Hynix Inc. (SKHYNIX / 000660.KS) is a South Korea-based memory semiconductor company and one of the world’s most important suppliers of High Bandwidth Memory (HBM) for AI accelerators. The company is the second-largest DRAM producer globally and a major NAND flash supplier, with a business model that spans memory chip design, wafer fabrication, advanced stacking, and packaging.

Unlike pure-play foundries that manufacture chips for external designers, SK Hynix designs and produces its own memory products across DRAM, NAND, and HBM. This gives the company exposure across the full memory value chain, from data center DRAM and enterprise SSDs to AI accelerator memory and mobile memory.

As of mid-2026, SK Hynix has become one of the most important bottlenecks in the global AI hardware stack. Its HBM3E and next-generation HBM4 products supply the high-speed memory needed for NVIDIA’s Hopper, Blackwell, Blackwell Ultra, and Vera Rubin GPU platforms, as well as custom AI accelerators developed by AI hyperscalers such as Google, AWS, and Microsoft. Its core markets include HBM for AI accelerators, DDR5 server memory, enterprise SSD and NAND flash, and mobile memory for smartphones and edge AI devices.

SK Hynix’s HBM Leadership and NVIDIA Vera Rubin Performance in Early 2026

SK Hynix started 2026 with one of the strongest earnings releases in semiconductor history. In Q1 2026, the company reported record revenue of approximately $34.1 billion (₩52.58 trillion), up 198% year over year, supported by surging HBM demand and stronger pricing across DRAM and NAND. HBM now accounts for more than 40% of total DRAM revenue, showing how quickly AI memory has reshaped SK Hynix’s business mix.

The bigger story was profitability. Operating profit reached approximately $24.4 billion (₩37.61 trillion), up 405% year over year, with an operating margin near 72%, even above NVIDIA’s 65% margin during the same period. For the rest of 2026, SK Hynix expects tight supply to continue, with HBM3E making up roughly two-thirds of HBM shipments while HBM4 ramps for NVIDIA’s Vera Rubin platform. The company plans around $20.5 billion in 2026 capex for HBM4 capacity and EUV expansion, with additional production expected from Cheongju M15X and Yongin through 2027.

Read More: Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle

SK Hynix’s 2026 Trading Strategy: Navigating the HBM Supercycle

To trade SK Hynix’s 2026 rally, investors need to balance three forces: whether key support levels hold, whether the market continues valuing SK Hynix as an AI infrastructure stock, and how much Korean market volatility affects the trade.

1. The $975 to $1,070 Zone Is the Key Support Floor

Technical analysts see the $975 to $1,070 per share (₩1,500,000 to ₩1,650,000) range as the key support zone, where the 50-day moving average overlaps with the prior breakout area from early Q2 2026. After the stock tested roughly $1,265 (₩1,949,000) in late May before consolidating, conservative traders may wait for support confirmation before adding exposure.

A decisive break below $975 (₩1,500,000) could signal a shift from AI growth-stock logic back toward traditional memory-cycle valuation, opening downside risk toward $780 (₩1,200,000).

2. The Main Valuation Debate Is AI Growth vs. Memory Cyclicality

The market is split on how to value SK Hynix. The bullish framework treats the company as an AI infrastructure stock, justifying higher multiples based on multi-year HBM demand from NVIDIA Vera Rubin and future AI platforms. The bearish framework treats it as a memory-cycle stock, arguing that margins and multiples could compress once supply catches up.

For swing traders, a volume-confirmed breakout above $1,170 (₩1,800,000) is important to avoid getting trapped in range-bound consolidation.

3. Korean Won and KOSPI Flows Can Amplify the Trade

SK Hynix trades in Korean Won and is highly exposed to USD/KRW moves, KOSPI fund flows, and Korean market risk. KOSPI is South Korea’s main stock market index, similar to the S&P 500 in the U.S., and it includes major Korean companies such as Samsung Electronics and SK Hynix. Because SK Hynix is one of the most important KOSPI stocks, it can move not only on HBM or earnings news, but also on broader Korean equity flows.

A weaker won can support USD-denominated revenue translation, but it can also trigger foreign fund outflows from Korean equities. Because SK Hynix often rotates against Taiwanese semiconductor exposure, position sizing should account for sharp currency-driven and index-driven swings, not just HBM fundamentals.

The SK Hynix 2026 Forecast: $1,300+ HBM Supercycle Upside vs. $780 Samsung Catch-Up Risk

SK Hynix’s 2026 outlook depends on one core question: can the company defend its HBM leadership as Samsung and Micron enter NVIDIA’s Vera Rubin supply chain? The bull case is built on multi-year AI memory demand, extreme DRAM tightness, and SK Hynix’s leading HBM4 allocation, while the bear case is that Samsung catches up faster than expected and forces a re-rating back toward traditional memory-cycle multiples.

Read More: Top AI Memory Stocks to Buy in 2026: DRAM, HBM, and AI Storage Demand Explained

The Bull Case: SK Hynix Breaks Above $1,300 on HBM Leadership

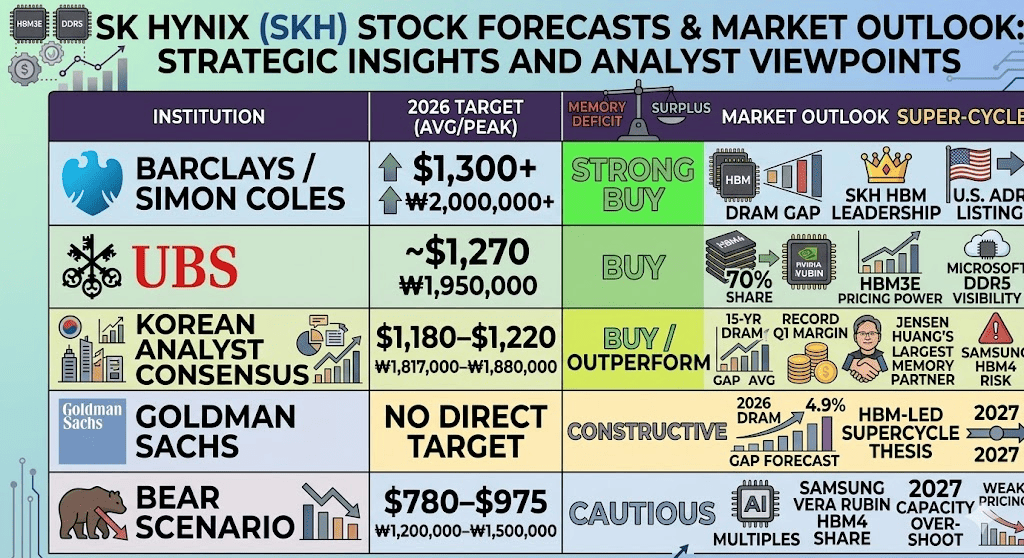

The bullish case depends on SK Hynix maintaining its HBM market share lead through the Vera Rubin ramp. Jensen Huang’s June 8 comment in Seoul naming SK Hynix as NVIDIA’s “largest memory partner,” combined with his “Please Make More” message at Computex 2026 in Taiwan, reinforced the market’s view that AI memory demand remains stronger than available supply. Barclays has raised price targets on continued memory tightness, while Korean analyst consensus sits around $1,180 to $1,220 per share (₩1,817,000 to ₩1,880,000).

Goldman Sachs’s 4.9% DRAM supply-demand gap forecast and supply-chain estimates that SK Hynix still holds 60% to 70% of NVIDIA Vera Rubin HBM4 volume support the premium valuation case. If SK Hynix protects its HBM lead, ramps its $20.5 billion capex without yield issues, and benefits from continued hyperscaler AI capex, the stock could move toward street-high targets above $1,300 per share (₩2,000,000), with aggressive bull cases pointing toward $1,430 (₩2,200,000) if a U.S. ADR listing attracts additional institutional capital.

The Base Case: SK Hynix Consolidates Between $1,070 and $1,235

The base case is a consolidation plateau. HBM demand remains strong through mid-2027, supported by NVIDIA Vera Rubin, Blackwell Ultra, and custom AI accelerators from Google, AWS, and Microsoft. However, the market also has to digest the new three-supplier reality: Samsung, SK Hynix, and Micron are all now certified for NVIDIA HBM4 supply.

This creates headline-driven trading conditions. Samsung’s HBM4 mass production and possible share gains could offset positive AI demand news, while SK Hynix’s reported decision to reduce 2026 HBM4 output by 20% to 30% in favor of higher-volume HBM3E adds execution complexity. Under this scenario, SK Hynix trades between $1,070 and $1,235 per share (₩1,650,000 to ₩1,900,000) as investors wait for clearer evidence on HBM4 share, pricing, and margins.

The Bear Case: SK Hynix Falls Toward $780 if Samsung Catches Up

The bearish case centers on Samsung catching up faster than expected. If Samsung raises its Vera Rubin HBM4 share toward 40% or higher in 2027, SK Hynix’s HBM dominance could compress, forcing the market to value the stock more like a cyclical memory producer again.

The second risk is capacity overshoot. SK Hynix’s $20.5 billion capex, Samsung’s large chip expansion budget, and additional DRAM capacity from China could create the conditions for a 2027 supply glut. If HBM pricing starts to correct in late 2026 or early 2027, the same operating leverage that drove SK Hynix’s profit surge could work in reverse, pulling the stock toward $780 per share (₩1,200,000) or lower.

Read More: Samsung Stock Price Prediction 2026: ₩480,000 Street-High Memory Supercycle or Strike Crisis Trap?

SK Hynix Price Forecasts for 2026 by Wall Street and Korean Analysts

|

Institution / Analyst |

USD Price Target |

KRW Price Target |

Market Outlook |

|

Barclays / Simon Coles |

$1,300+ |

₩2,000,000+ |

Strong Buy. Cites continued memory tightness, widening 2027 demand-supply gap, SK Hynix’s HBM leadership, and potential U.S. ADR listing as an additional catalyst. |

|

UBS |

~$1,270 |

₩1,950,000 |

Buy. Models roughly 70% HBM4 share for NVIDIA Vera Rubin, supported by HBM3E pricing power and Microsoft DDR5 supply visibility. |

|

Korean Analyst Consensus |

$1,180–$1,220 |

₩1,817,000–₩1,880,000 |

Buy / Outperform. Factors in the 15-year DRAM supply-demand gap, record Q1 operating margin, and Jensen Huang’s “largest memory partner” endorsement, partly offset by Samsung HBM4 share-gain risk. |

|

Goldman Sachs |

No direct target |

No direct target |

Constructive. Raised the 2026 DRAM supply-demand gap forecast to 4.9%, supporting the HBM-led memory supercycle thesis through 2027. |

|

Bear Scenario |

$780–$975 |

₩1,200,000–₩1,500,000 |

Cautious. Assumes AI growth multiples compress if Samsung captures meaningful Vera Rubin HBM4 share or if 2027 capacity overshoot weakens pricing power. |

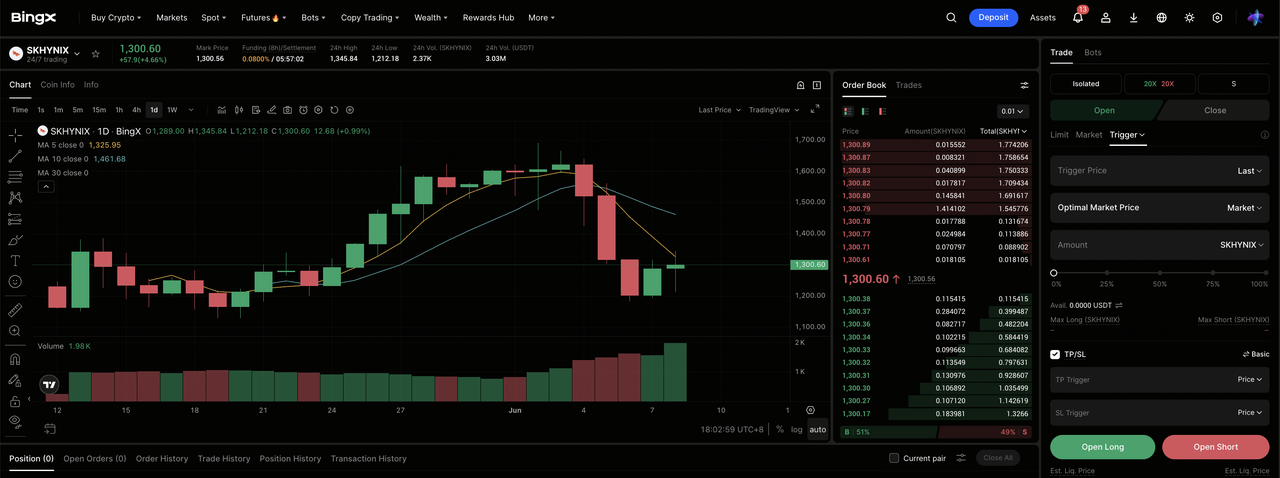

How to Trade SK Hynix (HXSCL) Stock Futures on BingX TradFi

As SK Hynix navigates this once-in-a-generation memory supercycle alongside the binary Samsung qualification risk, tactical traders can capitalize on its sharp bidirectional volatility through the BingX TradFi platform.

- Access BingX TradFi: Navigate to the specialized TradFi section on the main BingX exchange dashboard.

- Select SK Hynix (HXSCL): Search for and select the HXSCL-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the HBM supercycle, NVIDIA Vera Rubin ramp, Jensen Huang's "largest partner" endorsement, and Microsoft DDR5 contract will drive the equity toward street-high targets above $1,300 per share. Select Open Short to capitalize on potential Samsung HBM4 share-gain news or post-cycle capacity overshoot pullbacks.

- Select Leverage and Margin Mode: Apply your preferred Isolated or Cross-Margin parameters alongside disciplined leverage ratios to maximize capital efficiency while controlling liquidation risk.

- Execute Strict Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in profits and shield capital from sudden overnight gap events tied to Korean market open volatility, NVIDIA earnings, and Samsung HBM4 share-allocation headlines.

Top 5 Risks to Consider Before Investing in SK Hynix Stock

SK Hynix’s HBM leadership is one of the strongest AI memory stories in 2026, but the stock also carries meaningful downside risks. Investors should watch competition, capacity expansion, NVIDIA ramp timing, geopolitical exposure, and capital intensity.

- Samsung HBM4 Share-Gain Risk: Samsung’s certification for NVIDIA Vera Rubin HBM4 supply is the biggest competitive risk for SK Hynix. If Samsung’s allocation rises beyond the current 25% to 30% estimate, SK Hynix’s premium valuation could compress quickly as the market shifts from AI growth-stock logic back toward cyclical memory logic.

- Memory Cycle Reversal and Capacity Glut: SK Hynix’s $20.5 billion capex, Samsung’s major chip expansion budget, and new DRAM capacity from China could create oversupply risk in 2027. If HBM pricing corrects, the same operating leverage that drove SK Hynix’s profit surge could reverse sharply.

- NVIDIA Vera Rubin Ramp Risk: SK Hynix’s HBM4 revenue depends heavily on NVIDIA’s Vera Rubin platform ramping smoothly. Any delay from TSMC CoWoS packaging constraints, production hiccups, or downstream AI server bottlenecks could push out HBM4 revenue recognition and force more reliance on HBM3E.

- China Export Controls and Geopolitical Risk: SK Hynix operates meaningful fabrication capacity in China, exposing it to U.S. export controls, equipment restrictions, and broader geopolitical risk. Any tightening around advanced semiconductor equipment or licensing could disrupt operations, especially in NAND-related production.

- Capital Intensity and Currency Risk: SK Hynix’s 2026 capex plan is extremely large even by semiconductor standards. Combined with Korean Won volatility, any unexpected revenue slowdown could pressure margins, amplify earnings swings, and make the stock more sensitive to foreign fund flows and balance sheet concerns.

Final Thoughts: Is SK Hynix Stock a Buy in 2026?

As of June 2026, SK Hynix (SKHYNIX) is one of the clearest AI infrastructure plays in the global semiconductor supply chain. Its 72% Q1 operating margin, estimated 60% to 70% share of NVIDIA Vera Rubin HBM4 supply, three-year Microsoft DDR5 agreement, and the Goldman-flagged 15-year DRAM supply-demand gap all point to a company benefiting directly from the AI memory bottleneck. Jensen Huang’s description of SK Hynix as NVIDIA’s “largest memory partner” reinforces the bull case that HBM demand remains structurally stronger than supply.

The risk is valuation discipline. SK Hynix has already re-rated sharply, and memory remains a historically cyclical business. Samsung’s HBM4 ramp after NVIDIA certification will be the key catalyst to watch: if Samsung gains share faster than expected, SK Hynix could face multiple compression and a return to cyclical-memory valuation logic. For active traders, SK Hynix stock futures on BingX TradFi offer a high-volatility way to trade the HBM cycle; for longer-term investors, waiting for clearer evidence on Samsung’s Vera Rubin volume share and 2027 supply conditions may be more prudent.

Related Reading

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle

- Top AI Memory Stocks to Buy in 2026: DRAM, HBM, and AI Storage Demand Explained

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom