In late June 2026, Dell Technologies (DELL) finds itself positioned at a thrilling market crossroads between hyper-accelerated enterprise data center demand and aggressive executive liquidations. Following a historic 32.7% vertical breakout session at the end of May 2026, the Texas-based technology titan is currently trading near $427.78, boasting an incredible 234.7% gain year-to-date.

While the stock spent previous years categorized as a stable, single-digit growth personal computer and legacy hardware manufacturer, back-to-back operational milestones have totally transformed its valuation model. Investors are aggressively evaluating an exceptionally strong fiscal 2027 first-quarter earnings report and upgraded $167 billion full-year revenue expectations against an intense wave of open-market insider sales that has topped $1.7 billion over the past three months alone.

As the global computing ecosystem transitions toward sovereign private data centers and complex generative AI workloads, the absolute necessity for massive GPU system integration has turned Dell into a primary hardware bottleneck. However, a persistent profit-taking sequence from senior management and key institutional stakeholders has introduced a unique structural overhang.

This guide breaks down the Dell Technologies stock forecast and price prediction for the remainder of 2026, utilizing data from Morgan Stanley, Bank of America, Goldman Sachs, GuruFocus valuation models, and official regulatory filings.

You will also discover how to trade Dell Technologies (DELL) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Dell (DELL) Traders to Know in 2026

As Dell navigates a high-stakes environment of hardware allocation scaling and evolving enterprise IT budgets, traders must closely monitor these five market-moving factors:

- The 757% AI Server Revenue Explosion: In its latest fiscal Q1 2027 earnings print, Dell's infrastructure division delivered an astronomical 757% year-over-year revenue increase in dedicated AI servers, scaling directly to $16.1 billion for the quarter.

- The $1.7 Billion Insider Selling Wave: Over the past three months, Dell corporate insiders have executed zero open-market purchases while liquidating an aggregate $1,726.4 million ($1.72 billion) in shares, raising notable flags regarding short-term local price peaks.

- Raised $60 Billion AI Annual Guidance: Driven by an extensive hardware pipeline, COO Jeff Clarke formally upgraded Dell’s fiscal 2027 AI server revenue targets to $60 billion, highlighting that overall corporate revenue could grow 50% this year to $167 billion.

- Supply-Gated Backlog Extending into 2028: Management confirmed that enterprise order visibility now stretches through late 2026 and into 2028. Near-term revenue is no longer restricted by customer demand, but strictly by component supply and Nvidia GPU allocations.

- The Generative AI PC Refresh Moat: Beyond the data center, Dell’s Client Solutions Group is capitalizing on an aggressive commercial upgrade cycle. AI-enabled PCs are projected to make up 55% of the total global PC market by the end of 2026.

What Is Dell Technologies (DELL)?

Dell Technologies Inc. (NYSE: DELL) is a premier global provider of end-to-end digital infrastructure, enterprise hardware, and consumer technology solutions. Founded by Michael Dell, the company has successfully transitioned from its legacy roots as a dominant personal computer vendor into the world’s leading system integrator for high-performance scale-out architectures.

As of mid-2026, Dell represents the critical operational bridge between advanced semiconductor fabricators and real-world corporate data centers. Rather than designing custom silicon chips, Dell’s structural advantage lies in premium systems engineering. The company integrates complex graphics processing unit (GPU) clusters, such as Nvidia's H200 and Blackwell architectures, into robust PowerEdge server systems equipped with custom liquid cooling, storage attach layers, and proprietary enterprise software contracts.

Dell's Performance in Early 2026: The AI Server Re-Rating

DELL stock YTD performance as of June 2026 | Source: Yahoo Finance

The company kicked off the mid-part of 2026 by reporting blowout financial results that shocked Wall Street desks. Total quarterly revenue soared nearly 88% year-over-year to hit $43.84 billion, completely crushing consensus expectations of $35.77 billion. Backed by explosive operating leverage, adjusted non-GAAP earnings per share (EPS) arrived at $4.86, soundly beating the $2.94 analyst estimate.

This financial acceleration was spearheaded by Dell's Infrastructure Solutions Group (ISG), which logged record revenue as traditional servers and external storage platforms also grew 92% to $8.5 billion alongside the core AI line. Despite concerns that low-margin server integration would erode corporate profitability, Dell’s attach strategy, bundling high-margin proprietary storage networks like the new PowerStore Elite platforms, successfully lifted ISG operating margins to 10.5%. Concurrently, the company generated immense free cash flow, returning over $1.5 billion directly to shareholders in the form of aggressive stock buybacks and a declared $0.63 quarterly dividend.

Dell's 2026 Trading Strategy: How to Navigate Volatility in DELL Stock

Successfully navigating a mega-cap tech equity undergoing a fundamental valuation re-rating requires traders to balance clear momentum signals against macroeconomic headwinds and trailing structural valuations.

1. Watch the $385 - $400 Technical Gap-Fill Zone

Following its late-spring earnings breakout, technical analysts track the $385 to $400 window as a vital historical demand floor. On a short-term basis, the stock remains technically overbought, trading above its 50-day Simple Moving Average ($286.25) and 200-day Simple Moving Average ($174.87). As long as DELL respects the $410 intermediate Fibonacci support on daily closes, the immediate structural path remains firmly bullish.

2. Evaluate Trailing Multiples vs. Forward Revenue Certainty

Trading at a trailing P/E ratio of roughly 34x, DELL looks superficially expensive relative to its historical 5-year median P/E of 17.8x. However, macro traders are assigning a premium multiple due to structural backlog visibility. Because Dell's AI server deliveries are booked solid through late 2026, cyclical hardware demand risks are significantly lower for the next 12 to 18 months.

3. Monitor Component Cost Drag and Gross Margins

While demand is secure, gross margins, currently sitting at 23.8%, must be tracked continuously. Rising memory costs (DRAM and high-bandwidth memory components) threaten to squeeze system integration margins. Traders must verify whether Dell can cleanly pass these rising supply costs onto enterprise buyers in upcoming quarterly reviews.

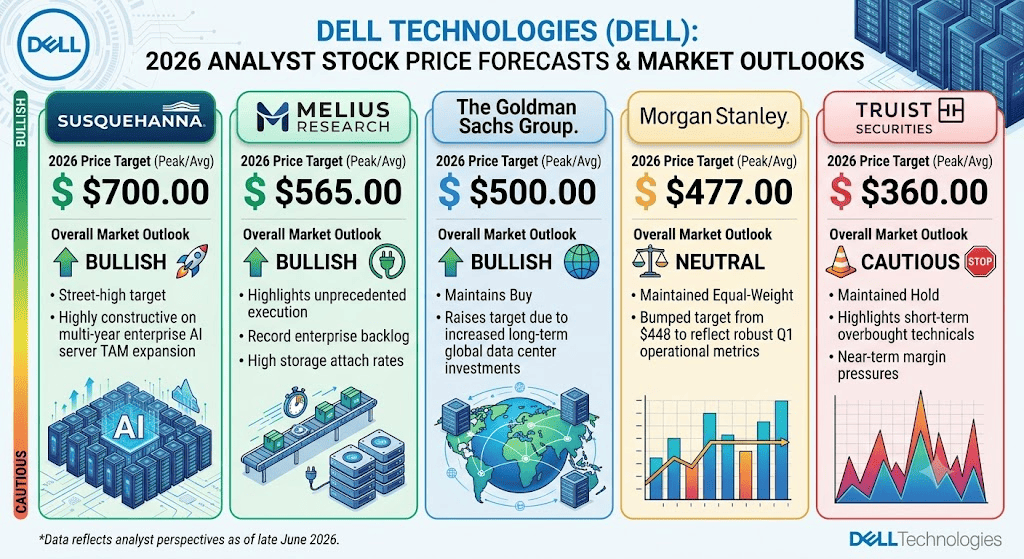

Dell 2026 Stock Forecast: $700 Street-High Peak vs. $213 Floor Trap

Dell stock predictions for 2026 by Wall Street analysts

Evaluating Dell's forward trajectory requires looking past short-term retail hype and mapping out realistic bull, base, and bear scenarios.

Dell's Bull Case: The $700+ Hyperscaler Integration Monopoly

The bullish thesis hinges on flawless backlog conversion and structural margin expansion. Championed by aggressive street-high targets from firms like Susquehanna's $700, this path assumes that Dell secures unhindered GPU allocations from Nvidia while scaling its high-margin APEX subscription-based infrastructure models. In this scenario, Agentic AI trends will trigger a massive parallel update cycle for standard corporate CPUs and edge devices. If Dell easily exceeds its fiscal revenue guidance and drives operating margins toward 12%, the stock will likely undergo another major multi-day extension, pushing past $500 toward the maximum street target.

The Base Case for DELL Stock: $440 – $500 Consolidation Plateau

The base case envisions a steady consolidation phase where the market matches Dell’s immense revenue generation against its heavy insider liquidation overhang. Under this framework, full-year revenue cleanly hits the projected $165 billion to $169 billion corridor, and AI server revenues reach the promised $60 billion mark. However, the equity faces a structural valuation cap due to persistent institutional profit-taking and competitive cross-winds from rival firms like Super Micro and HPE. This favors a highly liquid, range-bound pattern hitting average analyst price targets near $490.

DELL's Bear Case: The $213 Supply Chain and Margin Squeeze Trap

The bearish outlook focuses on hardware commoditization and macro tightening. If memory component costs spike aggressively or if hyperscaler clients choose to build proprietary data center racks rather than utilizing Dell as a system integrator, gross margins will take a direct hit. This risk is compounded if a cooling macroeconomy prompts Fortune 500 IT departments to freeze capital expenditure budgets. A decisive breakdown below the $385 gap-fill support floor would invalidate the structural uptrend, exposing DELL to a deep mean-reversion correction down toward its more cautious historical support lines near $213.

Dell Technologies (DELL) Price Predictions for 2026 by Wall Street Analysts

The table below details the mid-2026 analyst adjustments following Dell’s recent financial repricing:

|

Institution |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

Susquehanna |

$700.00 |

Bullish: Street-high target; highly constructive on multi-year enterprise AI server TAM expansion. |

|

Melius Research |

$565.00 |

Bullish: Highlights unprecedented execution, record enterprise backlog, and high storage attach rates. |

|

The Goldman Sachs Group |

$500.00 |

Bullish: Maintains Buy; raises target due to increased long-term global data center investments. |

|

Morgan Stanley |

$477.00 |

Neutral: Maintained Equal-Weight; bumped target from $448 to reflect robust Q1 operational metrics. |

|

Truist Securities |

$360.00 |

Cautious: Maintained Hold; highlights short-term overbought technicals and near-term margin pressures. |

How to Trade Dell Technologies (DELL) Stock Futures on BingX TradFi

DELL/USDT perpetual contract on BingX futures market

As Dell Technologies executes this high-volume public market breakout, tactical traders can cleanly capitalize on its price action through the BingX ecosystem.

- Access BingX TradFi: Head to the specialized TradFi section located on the main BingX exchange platform.

- Select Dell Technologies (DELL): Input and locate the specialized DELL-USDT perpetual futures contract window.

- Choose Your Direction: Select Open Long if you believe the $60 billion AI server target and AI PC refresh will drive the asset past its $490 consensus targets. Select Open Short to capitalize on heavy corporate insider selling and component margin compression.

- Select Leverage and Margin Mode: Set your targeted Cross or Isolated margin parameters alongside calculated leverage levels to manage capital efficiently.

- Enforce Strict Risk Protocols: Deploy advanced BingX Take-Profit and Stop-Loss (TP/SL) orders to shield your available trading margin from sudden multi-percentage intraday swings.

Top 5 Risks to Consider Before Investing in DELL Stock

Before entering a position in Dell, market participants must factor in these core structural risks:

- Massive Executive Profit-Taking: The liquidation of over $1.7 billion in stock by insiders over a 90-day window suggests that leadership views the equity as fully valued at current local levels.

- Severe GPU Allocation Dependencies: Dell's delivery timelines are entirely tethered to external chip fabricators. Any manufacturing delay or bottleneck at Nvidia instantly hits Dell's revenue generation.

- Hardware Margin Compression: System assembly and integration carry structurally lower gross margins than software or pure chip design, making Dell vulnerable to raw component price volatility.

- Intense Enterprise OEM Competition: Dell faces aggressive, hyper-focused competition in scale-out server deployment from rivals like Super Micro Computer (SMCI) and Hewlett Packard Enterprise (HPE).

- Macroeconomic Capital Cycles: A sudden economic downturn or elevated interest rate landscape could compel corporate IT departments to defer non-essential server infrastructure upgrades.

Final Thoughts: Is Dell Technologies (DELL) Stock a Buy in 2026?

As of June 2026, Dell Technologies stands as one of the most dominant and fundamentally sound structural plays of the global artificial intelligence infrastructure buildout. The company's ability to drive multi-billion dollar revenue expansions while securing a visible backlog extending out to 2028 proves it is an essential engine of modern corporate cloud computing.

However, trading an asset that has surged over 230% YTD while experiencing major corporate insider distributions demands strict portfolio discipline. For short-term momentum traders, the stock offers an unparalleled environment for high-liquidity volatility capture via BingX futures. Long-term market participants may find it highly effective to wait for key technical pullbacks toward structural gap-fill zones, ensuring that localized profit-taking cycles are fully absorbed before deploying long-term investment capital.

Risk Reminder: Trading mega-cap technology equities during rapid valuation re-ratings involves significant financial risk due to elevated beta metrics, supply chain variations, and sudden institutional reallocation waves. Always leverage disciplined risk protocols, precise positioning sizes, and mandatory stop-losses.

Related Reading

- Infleqtion Stock Price Prediction 2026: $22 CHIPS Boom or Insider Selling Trap?

- IBM (IBM) Stock Outlook for 2026: Quantum Leader or Legacy Victim?

- Ford Stock Price Prediction 2026: $20 Data Center Battery Boom or Legacy Recall Trap?

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle