Amazon (AMZN) enters the second quarter of 2026 navigating a high-stakes transition. While the stock has retreated 17% from its 2025 all-time high of $253.46, the company is doubling down on its AI-First infrastructure, committing a staggering $200 billion in capital expenditures (CapEx) for 2026. With AWS revenue growth re-accelerating to 24% and the scaling of in-house Trainium3 silicon aimed at reducing dependency on third-party GPUs, Amazon is betting its $2.1 trillion valuation on becoming the primary backbone for enterprise generative AI. Explore the institutional price targets for Amazon stock in 2026, the impact of US trade policy, and whether AMZN is a buy-the-dip opportunity at 25x forward earnings.

In early 2026, Amazon (AMZN) signaled that its massive investment cycle into artificial intelligence is no longer speculative, but is now also a matter of physical capacity. Despite market skepticism regarding a temporary decline in free cash flow, Amazon’s core profit engines of AWS and Advertising remain formidable, with trailing-12-month operating cash flow hitting a record $139.5 billion. As of March 2026, the narrative has shifted from retail logistics to Infrastructural Dominance: how quickly Amazon can install and monetize data center capacity to meet an unquenchable demand for AI workloads.

Amazon faces a structural crossroads. CEO Andy Jassy has dismissed concerns over the $200 billion CapEx plan, noting that AWS is monetizing capacity as fast as it can be installed. While a hawkish Federal Reserve holds rates at 3.50%–3.75% and a global oil spike over $100/barrel have pressured consumer-facing retail margins, the underlying re-acceleration of the cloud business suggests the fundamental floor remains robust.

This guide breaks down the Amazon stock price prediction for 2026 using data from Barclays, Evercore ISI, and Jefferies. You will also discover how to gain exposure to Amazon (AMZN) stock futures through BingX TradFi and via Ondo's tokenized Amazon stock AMZNON on BingX spot market.

Top 5 Things for Amazon Investors to Know in 2026

- The $200B Bet: Management’s guidance for $200 billion in 2026 CapEx is aimed at AI infrastructure and satellites, representing a 51% increase year-over-year.

- AWS Re-acceleration: Cloud revenue growth jumped to 24% in Q4 2025, with institutional bulls like Citi expecting this to hit 28-29% later in 2026.

- Silicon Sovereignty: Amazon’s custom AI chips, Trainium and Graviton, now exceed $10 billion in annualized revenue, offering superior unit economics for AI inference.

- Advertising Powerhouse: Advertising revenue reached $21.3 billion in Q4 2025, up 22% YoY, emerging as a critical high-margin offset to retail shipping costs.

- Trade Policy Headwinds: Lingering concerns over US trade tariffs continue to weigh on third-party seller margins, creating a valuation discount relative to historical means.

What Is Amazon (AMZN)?

Amazon is the world’s largest e-commerce retailer and the leading provider of cloud infrastructure (AWS). In 2026, it has evolved into a Triple Threat platform: a dominant retail ecosystem, a global AI infrastructure provider, and a high-growth digital advertising network. Its value lies in its Flywheel Effect, where AWS profits and Advertising margins fund the massive capital outlays required to dominate the next era of computing. Unlike specialized AI firms, Amazon owns the entire stack, from custom silicon and data centers to the consumer-facing interface and logistics network.

Amazon's Strategic Evolution (1997–2026): From Bookseller to AI Utility

- The E-commerce Expansion (1997–2014): Disrupting traditional retail, scaling Prime, and building the world's most sophisticated logistics network.

- The Cloud Dominance Era (2015–2023): AWS becomes the primary profit driver, subsidizing retail growth and establishing Amazon as the operating system of the internet.

- The Generative AI & Silicon Era (2024–2026+): The current phase, focused on vertical integration. Amazon is now designing its own chips and building AI foundries to serve the massive compute needs of the 2030s.

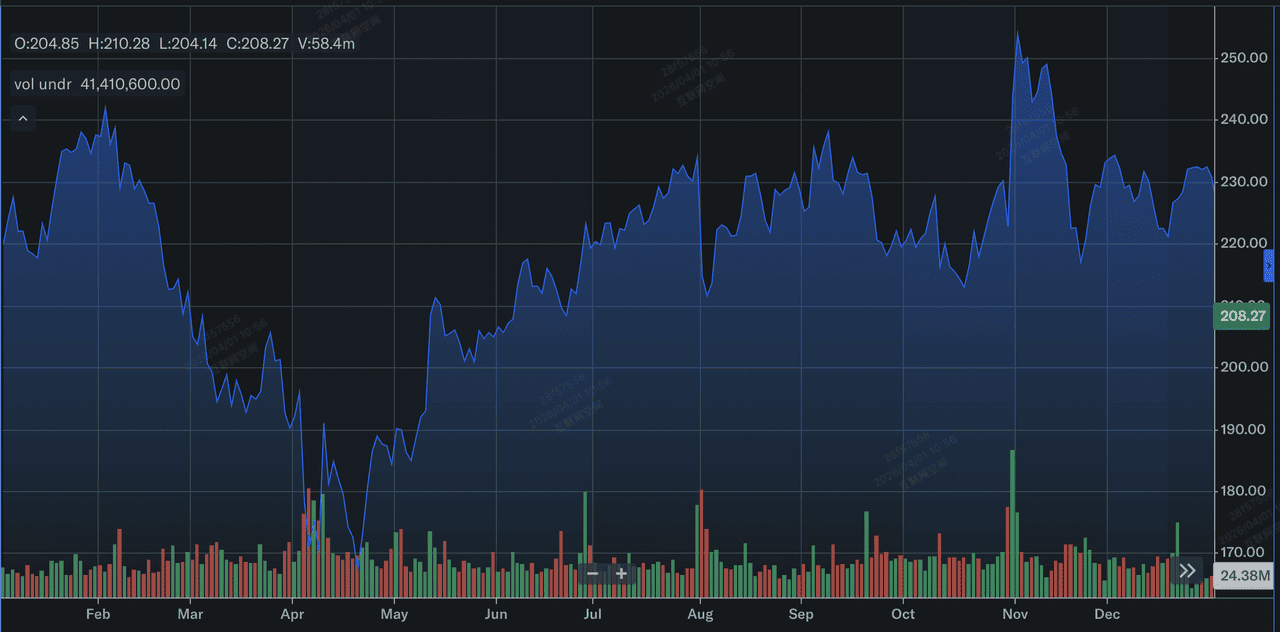

Amazon (AMZN) 2025 Performance Overview: The Trough Before the Surge

Amazon stock performance in 2025 | Source: Yahoo Finance

In 2025, Amazon demonstrated that while its top line is resilient, its valuation is sensitive to the timing of its capital returns.

- All-Time High Reached: AMZN shares touched a record $253.46 on November 3, 2025, driven by AI optimism and accelerating AWS spending.

- The February Correction: Following the Q4 earnings report on February 5, 2026, the stock plunged 17% as investors balked at the massive $200 billion infrastructure budget.

- AWS Backlog Growth: Despite the share price dip, the AWS revenue backlog climbed to $244 billion, a 40% growth YoY, signaling massive future revenue.

- Advertising Integration: Prime Video’s ad-supported model reached 315 million global viewers, turning streaming content into a meaningful profit contributor.

The Amazon Thesis for 2026: 4 Key Drivers of $AMZN Stock Valuation

Amazon's 2026 valuation hinges on the successful convergence of infrastructure expansion, high-margin revenue streams, and a structural pivot toward in-house artificial intelligence efficiency.

- Monetizing AI Capacity: Amazon is experiencing supply-constrained demand. If they can deploy Trainium3 chips by mid-2026, they can capture higher margins than rivals relying solely on external GPUs.

- The 15% Margin Target: TIKR models suggest that as the current CapEx cycle matures, net income margins could expand to 15% by 2030, up from 10.8% today.

- Retail Efficiency: Advances in robotics and a shift to everyday essentials (1 in 3 units sold) are stabilizing the retail segment despite inflationary pressures.

- AWS Run Rate Vision: CEO Andy Jassy predicts AWS can reach an annual run rate of $600 billion, driven by AI-native enterprise migrations.

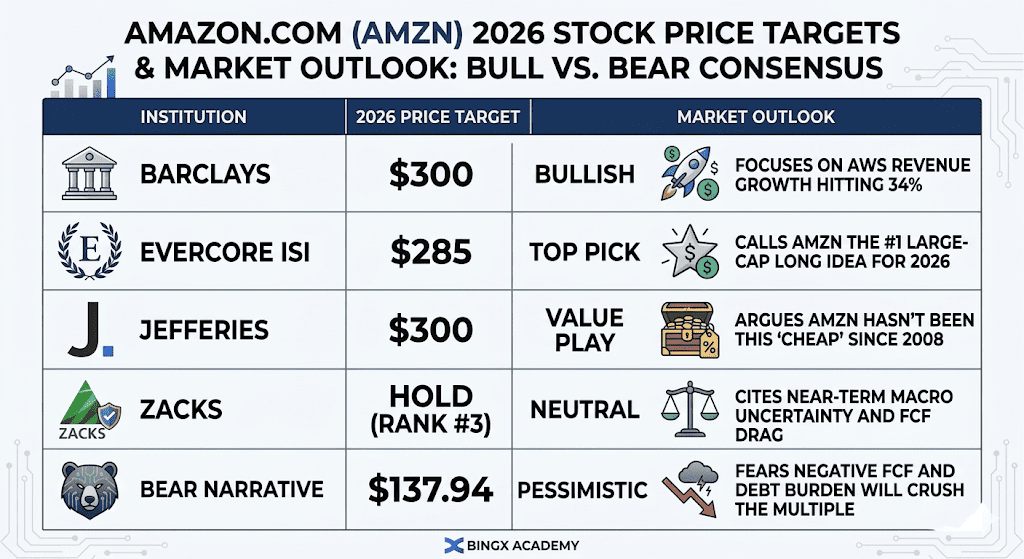

Amazon Stock Price Forecasts for 2026: Bull vs. Bear Outlook

Amazon stock outlook for 2026 | Source: Various analysts

The divergence in Amazon’s 2026 valuation reflects a high-stakes debate between those betting on an AI-driven cloud supercycle and those wary of the massive capital commitments required to sustain it.

The Bull Case: The $300 Efficiency Explosion

The bull narrative is predicated on a significant valuation re-rating as the market realizes Amazon is trading at a trough multiple of 10.3x forward EBITDA, a level not seen since the 2008 financial crisis. Institutional bulls like Barclays and Jefferies argue that the $200 billion CapEx cycle is not a cost burden but a high-return moat-building exercise. If AWS growth sustains at or above 25% through the Q1 2026 earnings call, it confirms that Amazon is successfully monetizing AI capacity as fast as it installs it. In this scenario, the stock moves toward $300 as the market stops valuing AWS as a mature retailer and starts pricing it as the primary infrastructure layer for global generative AI.

Practically, this scenario relies on the scaling of custom silicon like Trainium3, which offers superior unit economics by reducing reliance on external GPUs. If Trainium and Graviton revenues, already at a $10 billion annual run rate, continue to grow at triple digits, Amazon’s margins will likely expand even as spending remains elevated. For investors, the buy-the-dip opportunity is justified by the sheer scale of the profit engine, with $139.5 billion in trailing operating cash flow providing a massive liquidity cushion that most competitors cannot match.

The Base Case: The $240 Wait-and-See Consolidation

The base case envisions Amazon as a high-performing Cash Cow navigating a transition year where stock performance tracks steady operational gains rather than multiple expansion. In this outlook, AWS revenue growth remains stable between 20% and 23%, supported by a robust $244 billion backlog, but bottom-line growth is tempered by rising depreciation costs from the 2025–2026 data center build-out. While the retail segment continues to gain market share in everyday essentials, higher shipping costs due to $100+ oil prices act as a persistent ceiling on net income growth.

Under this scenario, the stock likely oscillates between $220 and $250, tracking the broader S&P 500 tech recovery. Investors focus on the free cash flow trough, accepting a temporary dip into negative territory as a necessary trade-off for future dominance. This scenario assumes that while AI monetization is active, it has not yet reached the tipping point required to trigger a full-scale rally to all-time highs. The 25x forward P/E remains stable as the market waits for more tangible evidence that the $200 billion bet will translate into 15%+ net margins by 2030.

The Bear Case: The $140 Structural Reset

The bear case is driven by infrastructure exhaustion and a potential mismatch between supply and demand. If the $200 billion investment fails to yield a proportional spike in AWS revenue, specifically if growth slips below 20%, concerns over unsustainable spending will dominate the narrative. Bears, including analysts at Bears of Wall Street, point to a mounting debt burden, which now exceeds $73 billion, and the risk of negative free cash flow reaching $28 billion by year-end. If AI monetization takes longer than expected, Amazon’s status as a premier cash generator could be called into question, leading to a massive institutional de-risking event.

External macro pressures exacerbate this downside risk, particularly the double-whammy of $100/barrel oil and a hawkish Fed keeping borrowing costs high for both Amazon and its consumers. If the Strait of Hormuz closure or wider Middle East volatility continues to disrupt global supply chains, Amazon’s retail margins, already pressured by US trade tariffs, could collapse toward zero. In this uninvestable scenario, the stock could retreat toward its intrinsic value of $137.94, representing a 30%+ downside from current levels as the AI bubble fears gain traction.

Amazon (AMZN) 2026 Investment Outlook: The Infrastructure Pivot vs. FCF Pressure

|

Institution |

2026 Price Target |

Market Outlook |

|

Barclays |

$300 |

Bullish: Focuses on AWS revenue growth hitting 34%. |

|

Evercore ISI |

$285 |

Top Pick: Calls AMZN the #1 large-cap long idea for 2026. |

|

Jefferies |

$300 |

Value Play: Argues AMZN hasn't been this "cheap" since 2008. |

|

Zacks |

Hold (Rank #3) |

Neutral: Cites near-term macro uncertainty and FCF drag. |

|

Bear Narrative |

$137.94 |

Pessimistic: Fears negative FCF and debt burden will crush the multiple. |

How to Trade Amazon (AMZN) Stock on BingX

Maximize your trading precision by leveraging BingX AI to analyze Amazon’s 2026 volatility patterns and automate your entry strategies across our diverse TradFi instruments.

Buy and Sell Amazon Ondo Tokenized Stock (AMZNON) on the Spot Market

AMZNON/USDT trading pair on the BingX spot market

- Log in to your BingX account and deposit USDT.

- Search for AMZNON/USDT in the Spot Market.

- Choose Market or Limit order and enter your investment amount.

- Confirm to hold fractional Amazon-linked assets.

Long or Short Amazon (AMZN) Stock Futures on BingX TradFi

AMZN/USDT perpetual contract on BingX futures market

- Navigate to BingX TradFi and select Stock Futures.

- Select the AMZN/USDT perpetual contract.

- Set your leverage (e.g., 2x–5x) and select Open Long or Open Short.

- Set TP/SL (take-profit/stop-loss) to protect against earnings-driven volatility.

5 Critical Risks to Watch for Amazon Investors in 2026

While Amazon’s AI-driven roadmap offers significant upside, investors must navigate a complex environment of massive capital outlays, evolving global trade policies, and intensifying cloud competition.

- CapEx Efficiency: If the return on $200 billion in spending takes longer than 18 months to materialize, the stock multiple will remain compressed.

- Trade Tariffs: New US trade policies could disrupt the cost structure of the 3rd-party seller marketplace, which accounts for the majority of units sold.

- Macro Inflation: Oil prices over $100/barrel increase shipping costs and reduce discretionary spending among Amazon’s core retail customers.

- AI Model Competition: AWS must prove that its Bedrock platform is as attractive as direct offerings from Microsoft's OpenAI or Google Gemini.

- Free Cash Flow Trough: Analysts expect FCF to turn negative in 2026; if this extends into 2027, credit ratings and buyback potential could be impacted.

Conclusion: Should You Invest in Amazon (AMZN) Stock in 2026?

Deciding to invest in Amazon in 2026 requires looking past near-term noise to focus on long-term earnings power. At roughly 25x forward earnings, Amazon is trading at a significant historical discount. The thesis for 2026 hinges on monetization velocity: if the massive build-out of data centers translates into a sustained 25%+ growth rate for AWS, the current pullback to around $200 will be viewed as a generational buy-the-dip moment.

However, for risk-averse investors, the transition to a negative free cash flow profile is a legitimate red flag. The April earnings report will be the first moment of truth for the $200 billion bet. If management provides clear guidance on an FCF trough and recovery, the path to $300 is wide open. If not, the stock may remain range-bound as the market demands proof of returns before awarding a higher valuation.

Risk Reminder: Trading and investing in equities like AMZN involves substantial risk. Amazon’s high capital intensity, combined with exposure to global trade volatility and AI competition, makes it a high-conviction but high-volatility asset. Always conduct independent research.

Related Reading

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Microsoft (MSFT) Stock Outlook for 2026: Can Azure AI and Copilot Growth Drive MSFT Stock to $550+?

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?

- Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?

- Alibaba (BABA) Stock Forecast for 2026: Can AI and Cloud Growth Push BABA Past $200?